Cash Pooling: A Practical Guide for Treasury Teams

As companies expand, treasury must manage cash not only with suppliers and customers but also between subsidiaries. One entity may need cash for payroll, another holds surplus funds, while a third is exposed to FX risk. Without a clear framework, these flows multiply into a web of transfers, FX costs, and reconciliation work.

With higher interest rates and stricter capital requirements, treasurers are under pressure to optimize liquidity across the group. Cash pooling has long been a core liquidity tool, but today’s rate environment has made it an even higher priority.

What is cash pooling?

Cash pooling centralizes liquidity across group entities, allowing treasury to manage cash at the group level instead of leaving balances idle in local accounts. The two main models are physical pooling and notional pooling.

Physical pooling (sometimes called cash concentration) involves the actual movement of funds. Surplus balances are swept from subsidiary accounts into a master account, often daily, while deficit accounts are funded from the same pool. This means a group can use its own cash to cover shortfalls instead of relying on external borrowing.

Notional pooling, by contrast, leaves funds in their local accounts but offsets them virtually. The bank aggregates the balances across all participating accounts and calculates interest on the net position. A positive balance in one entity reduces the cost of a negative balance in another, without physically moving the funds. This preserves local account structures and minimizes transfer costs while still reducing net borrowing at the group level.

The main difference is that physical pooling moves the money, while notional pooling moves only the interest calculation. Both aim to reduce idle cash and funding costs, but they come with different considerations: physical pooling requires intercompany lending arrangements and can raise tax questions, while notional pooling depends on the bank’s infrastructure and is not permitted in all jurisdictions.

Why do companies use cash pooling?

Reduce idle cash and borrowing costs

Pooling offsets surpluses and deficits across entities. This cuts overdraft interest where one unit is short while another holds excess funds.

Centralize processes and controls

By routing intercompany payments and sweeps through a central structure, treasury teams can apply consistent approval chains, strengthen oversight, and negotiate with banks or suppliers as a single entity.

Simplify reconciliation

With transactions concentrated in fewer accounts, matching bank records against ERP entries becomes faster and less error-prone, reducing manual work and audit risk.

Improve visibility

A pooled setup gives treasury a consolidated view of group liquidity, supporting more accurate forecasting and quicker allocation of funds to where they are needed.

Why traditional pooling setups fall short

Cash pooling can improve liquidity efficiency, but manual setups create new challenges:

Spreadsheets don’t scale

Many companies still rely on spreadsheets to track intercompany balances and cash positions. This approach is error-prone, lacks audit trails, and becomes harder to control as entities and accounts multiply.

Bank-led pooling is limited

Cash pooling is usually easier when all accounts sit within the same bank. Moving outside that network can make things trickier: some banks restrict pooling to their own accounts, others limit it to single currencies, and cross-bank setups are often more expensive and complex. As a result, adding new entities or changing providers can be difficult, which reduces flexibility as the business grows.

Regulatory scrutiny is increasing

Tax authorities are paying closer attention to cash pooling arrangements under transfer pricing rules. This means that companies need to document terms carefully, allocate interest fairly, and ensure compliance with OECD guidance and local tax laws.

A modern approach to intercompany liquidity

Treasurers are now adopting API-driven solutions that give them real-time control of intercompany liquidity. The focus is shifting from periodic cycles and static bank setups to automated, rules-based workflows integrated directly with ERP and payment systems.

Key practices in modern liquidity management include:

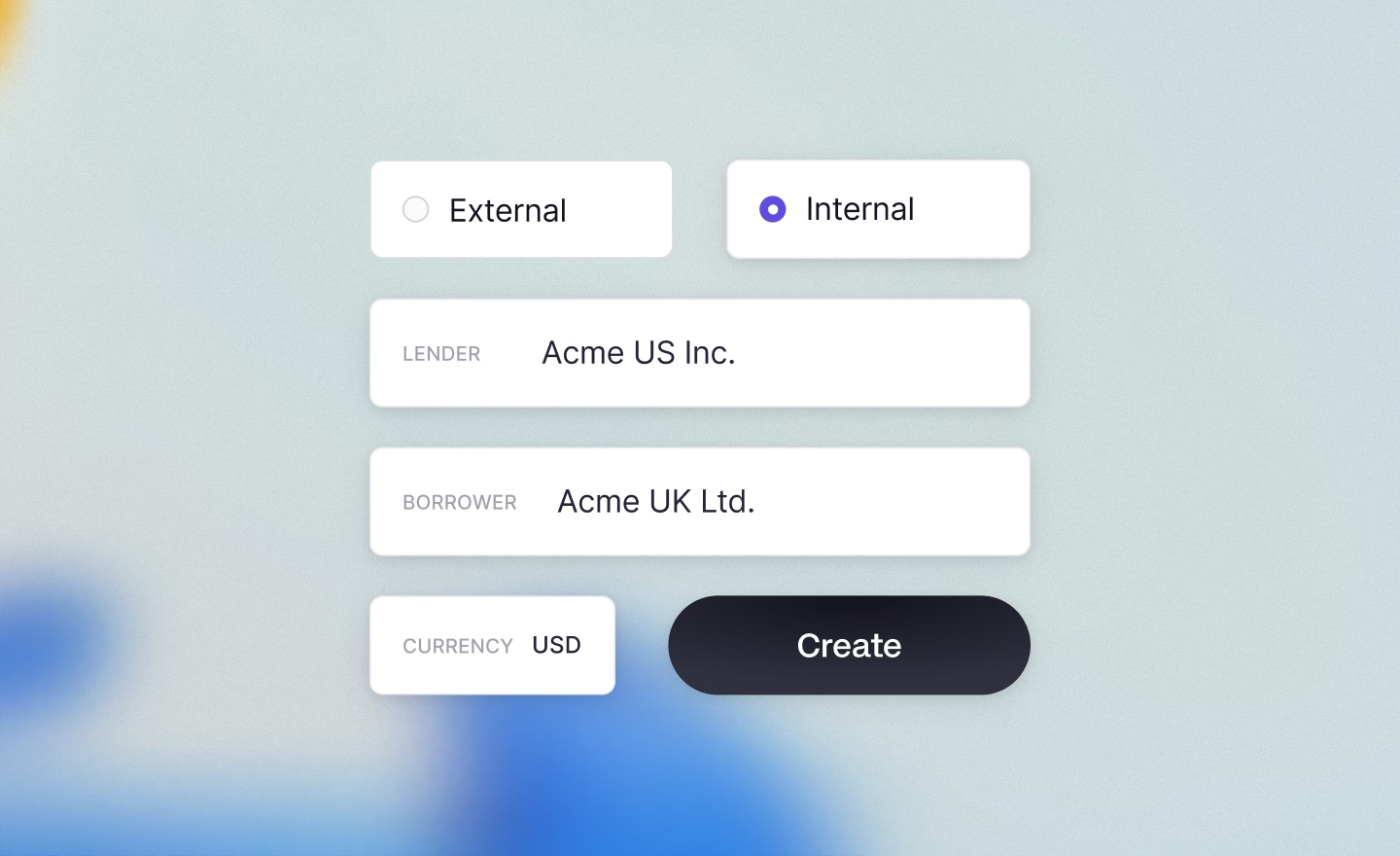

- Automated sweeps: Configure rules that move cash between entities as soon as balances cross set thresholds. This ensures subsidiaries remain funded while excess liquidity is consolidated centrally.

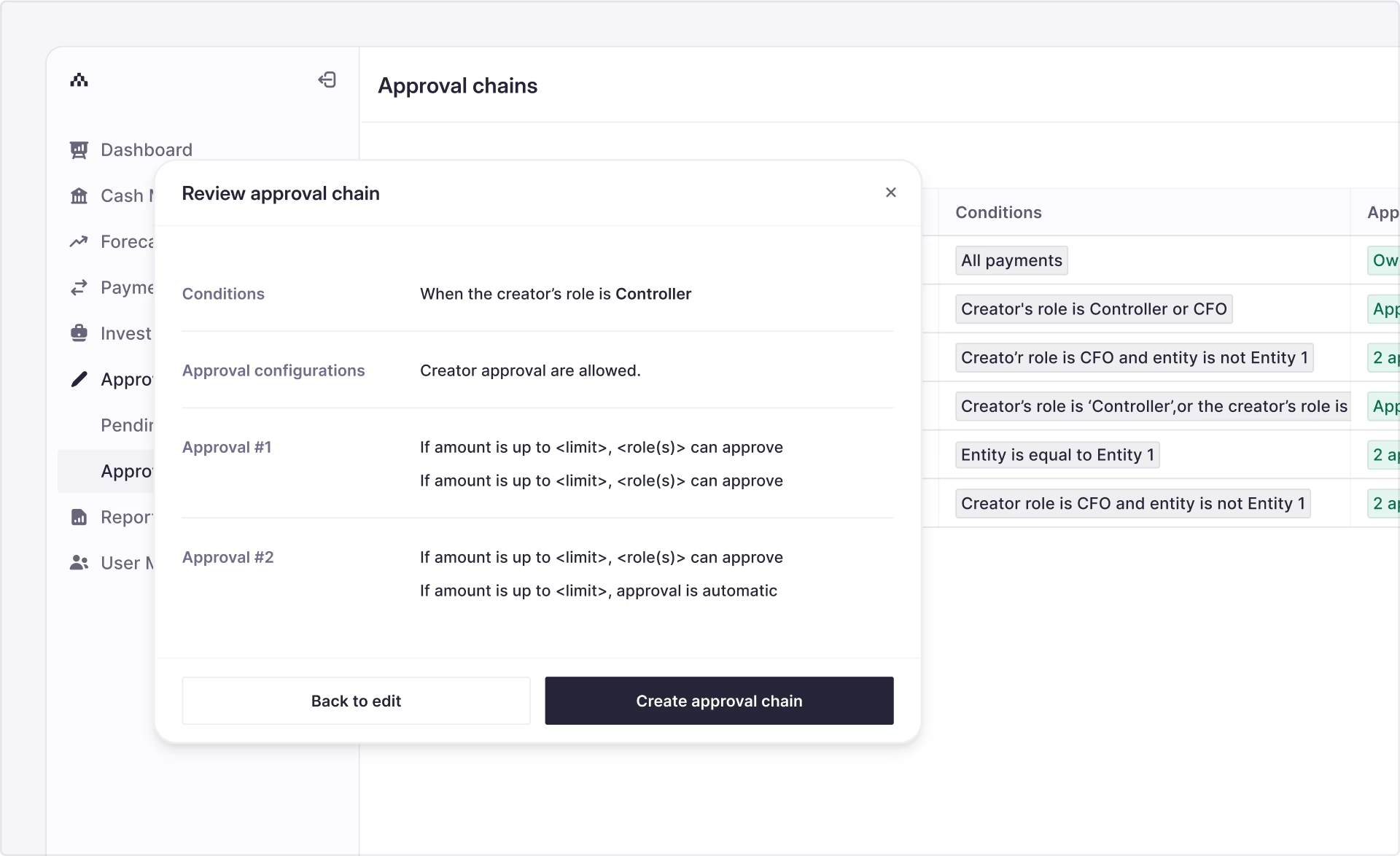

- Centralized payments and approvals: Treasury can initiate and approve intercompany transfers from a single platform, applying consistent approval chains and reducing fraud risk.

- Direct ERP–bank connectivity: Transactions flow automatically between banks and ERP systems, eliminating manual uploads and ensuring every transfer is booked in accounting without reconciliation delays.

- Embedded reconciliation and audit trails: Each transaction is tracked end-to-end, giving finance teams the transparency regulators expect and the audit evidence required for intercompany settlements.

- Data-driven oversight: With consolidated cash visibility, treasurers can map high-volume or high-FX-exposure entities, track key metrics such as idle balances or borrowing costs, and adjust rules in real time.

This shift reflects a broader trend in treasury: replacing manual, bank-led structures with automated, API-based processes that deliver efficiency, compliance, and control across the group.

How Atlar can help

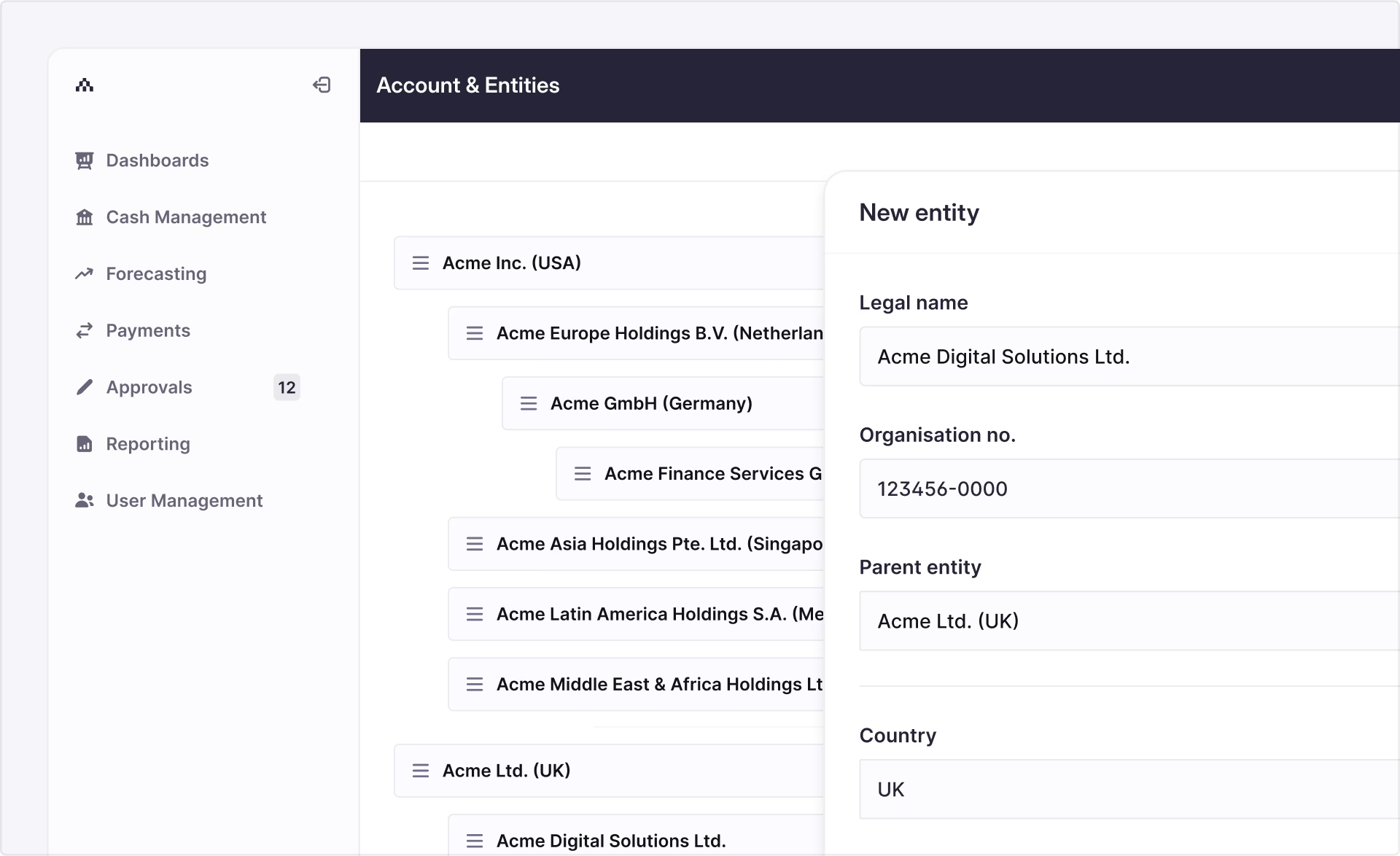

Atlar lets you centralize all of your bank accounts and cash positions in one platform, with built-in functionality for account grouping and entity management. Using the cash positioning feature, you can view balances at both entity and group level.

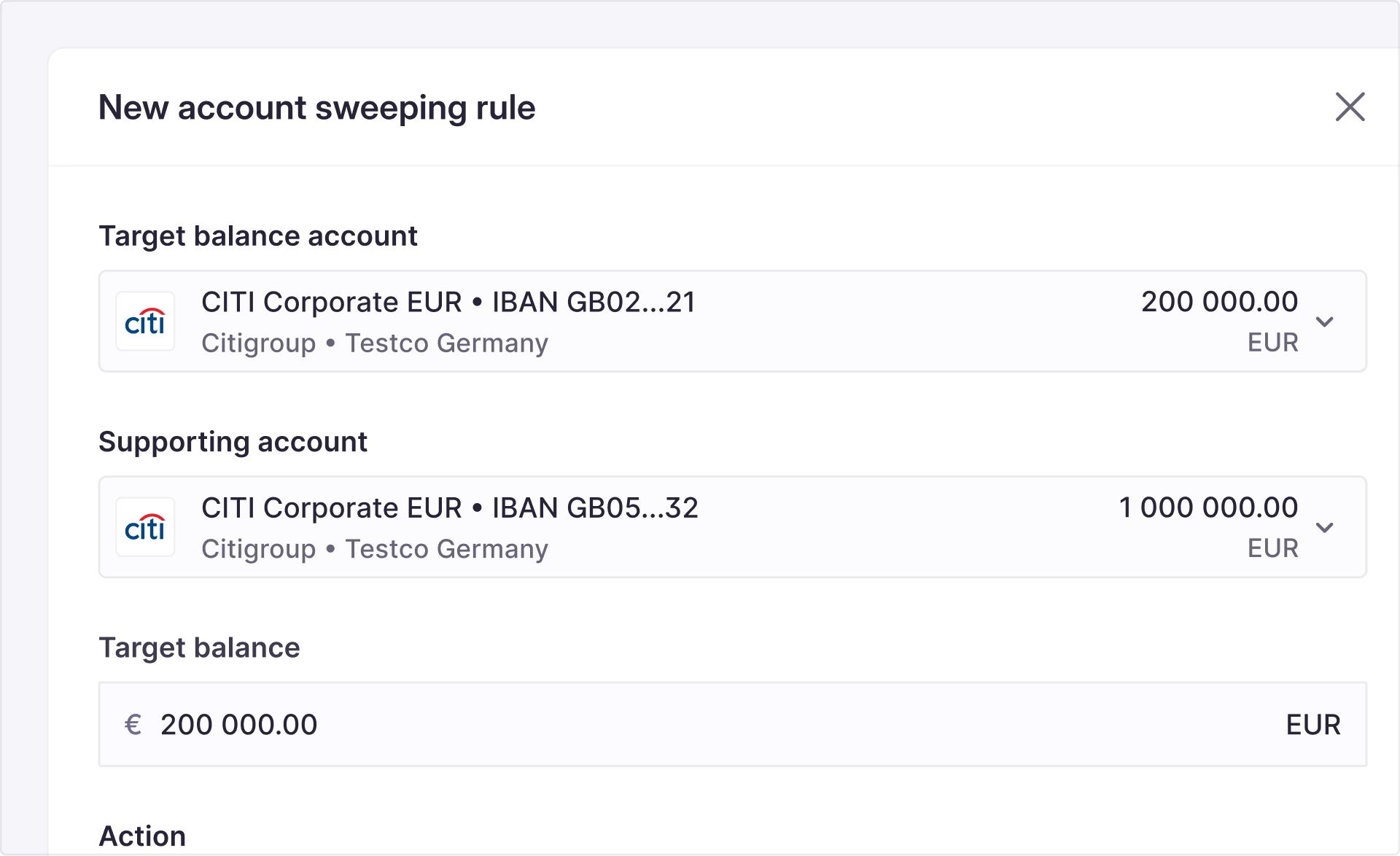

To support your cash pooling strategy, Atlar enables automated account sweeping. You can configure sweeping rules to transfer cash between accounts based on predefined thresholds, keeping subsidiaries funded and centralizing surplus liquidity. Monitoring alerts flag potential shortfalls or excess balances so treasury can act quickly.

Payments are managed end-to-end in one place rather than scattered across bank portals, while direct integrations with ERPs such as NetSuite and Dynamics ensure every settlement flows seamlessly into accounting. Real-time dashboards provide full visibility over multi-entity liquidity, combined with the audit trails and approval chains treasurers need to stay in control.

Customers like GetYourGuide and Acne Studios already use Atlar to manage liquidity across multiple entities, cutting manual work and increasing control. To see how your team can do the same, request a 30-minute platform demo.

_NEF-EDIT.avif)