Three Ways Companies Handle Bank Payments, and Why They Don't Work

A new breed of tech companies across a range of industries, from lending to insurance and marketplaces, have to process and reconcile large volumes of bank payments as a core part of their business. With payment needs shifting from batch-based to real-time, the technical and operational complexity is increasing as companies need to upgrade their infrastructure to manage bank payments efficiently.

Before Atlar

Until recently, businesses broadly had three options for managing bank payments at scale.

Scale a finance team

In the early days, companies often handled bank payments manually. That means having a finance team create and monitor transactions within a bank's online platform and match line items one by one with internal books. Alternatively, companies access banking services and reconcile bank statements via a legacy accounting software provider. These options offer a poor user experience and are prone to human error.

Things get increasingly complex as a growing company must deal with larger payment volumes, expand to new markets, and onboard new banking partners. At this stage, companies need to think of ways to automate bank payments.

Use a payment service provider (PSP)

PSPs sit in the flow of funds, meaning money moves through their bank accounts. They assist in holding customers' funds, initiating payouts, and accepting payments via an API. PSPs bear credit risk and take care of compliance on the customer's behalf.

Even so, PSPs come with several drawbacks. Many have limited geographical reach and are costly due to the bearing of credit risk. Companies can also lose control over their own onboarding and payment flows as PSPs conduct KYC checks and own more of the customer experience. Businesses will also have to weather slower receivables turnover due to rolling reserves and delayed settlement from PSPs.

Build custom integrations

As an alternative to using a PSP, some companies choose to build internal software that connects directly to banks' cash management channels, such as SFTP, EBICS, or via bank API.

Building bespoke integrations is time-consuming, requires significant engineering resources, and demands deep knowledge of banking and payments. Features such as approval workflows, audit trails, role-based access rights, counterparty management, and webhooks for real-time notifications all need to be baked in from the start. For most businesses, the opportunity cost of building this infrastructure internally is too high — it consumes capital, time, and diverts focus away from the core business.

Enter Atlar

Atlar removes the need to manually manage bank payments, pay substantial fees to PSPs, or spend engineering hours on non-core functionality. With fully managed, real-time bank connectivity and a platform built for payment automation, Atlar handles the complexity so finance teams can focus on what matters: running the business.

This is why leading companies including Trustly, Tide and Mangopay, rely on Atlar to manage payments across dozens of banks and entities.

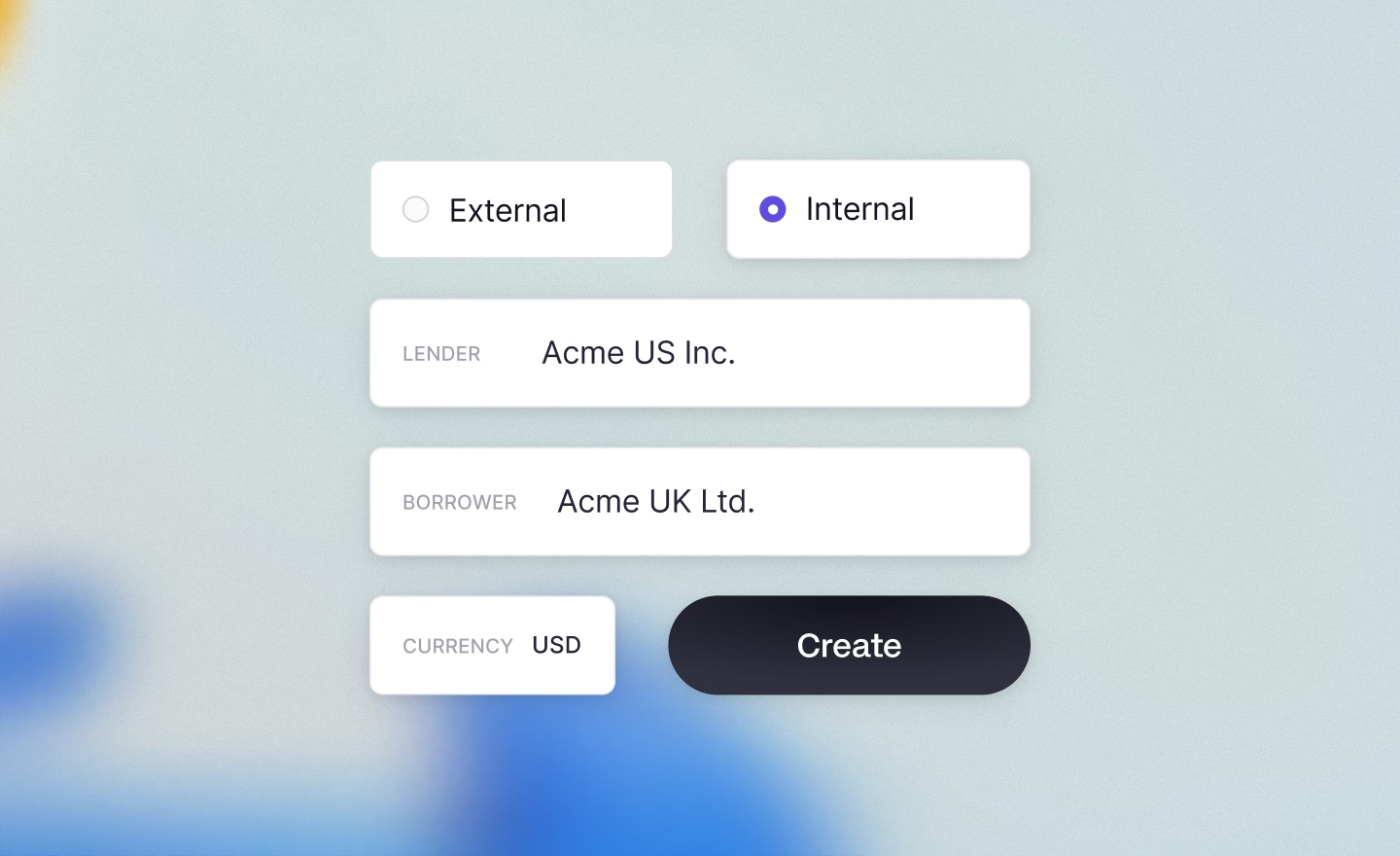

By connecting to the Atlar API, you can automatically initiate credit transfers and direct debits, monitor balances across bank accounts, and track payment status live via webhooks. AI-powered reconciliation then matches and verifies incoming payments across all your banks and entities, while native ERP integrations with NetSuite and Microsoft Dynamics keep your financial systems in sync.

The Atlar Dashboard gives finance teams real-time visibility over cash balances and cash flow across all accounts. Atlar Intelligence adds a layer of AI-native analysis, letting teams query payment data in natural language and surface insights without building manual reports.

Atlar is recognized as a NetSuite SuiteCloud International Partner of the Year and has earned 16 G2 badges for treasury and payment management, reflecting the platform's depth and customer satisfaction.

See it for yourself

Interested in automating your payment flows? Get in touch and we would be delighted to show you the platform in action.