Treasury Management Tooling Explained: From Excel to a TMS and Everything in Between

Introduction

Money is the lifeblood of business, a fact so obvious it almost goes without saying. This money can be held in a single account at your local bank or spread out over hundreds of accounts belonging to various entities, across dozens of financial institutions and in multiple currencies.

At its core, treasury management is the act of managing that money. This means making payments, understanding cash flow, freeing up working capital, investing excess cash, and creating financial reports for stakeholders. With money comes financial risk: managing a company’s exposure to fraud plus interest rate and foreign exchange (FX) volatility fall under treasury management too.

There are a few ways companies perform these activities:

- Manual processes using spreadsheets, bank portals, and file transfers

- Enterprise resource planning (ERP) software

- Treasury management systems (TMS)

- Modern, real-time platforms like Atlar

In this guide we dive deep into the options above, why businesses pick one over the others, and how to choose the right tooling for your business.

Overview of treasury tooling

Considering how easy it has become to manage money as a consumer, tooling for businesses has arguably not received the same level of investment. It’s still dominated by legacy systems and processes, often lacks modern integration capabilities, and requires manual work like file transfers.

One reason for this is complexity. Businesses need to connect a patchwork of banks, payment platforms, and internal systems to manage their money. Factor in multiple markets and currencies, regulation, and the need for near 100% uptime and you can appreciate why tooling has become highly sophisticated while real product innovation has slowed. With the cost of switching so high, businesses find themselves locked into providers and processes regardless.

Manual processes involving bank portals, spreadsheets, and file transfers have long been the only fallback option. These workflows, though time-consuming and prone to error, are preferred since the up-front cost of traditional treasury tooling is prohibitively high for most non-enterprise businesses. This leaves finance teams spending hours gathering and updating data every week while navigating the errors and security risks inherent in such processes.

Recently, new treasury management tooling has emerged that’s based on modern, cloud-native, and API-first technology, making it easier to implement and use. These platforms are also viable for a broader set of businesses, not only the largest enterprises, since they don’t require in-house specialists and extensive IT resources.

The demand for all types of treasury management software is growing, driven by regulatory requirements, the need for financial visibility, and automation. According to a study by Polaris Market Research, the total market value of treasury management software is expected to push $16 billion by 2032. Modern, cloud-based platforms are growing at the fastest rate and increasing their overall market share.

A timeline of treasury technology

Treasury management has long been technology-dependent. Here’s a brief timeline of its evolution up to the present and modern platforms like Atlar.

Swift network founded in 1973

The early 1970s saw the beginnings of the global, interconnected banking system we know today. Financial transactions became increasingly digitized and standardized internationally, making automated data processing possible and leading to the earliest treasury management services.

First spreadsheet program in 1979

The rise of the personal computer allowed spreadsheets to replace physical ledgers and books, making it easier to manage large amounts of financial data. Data collection and processing was still heavily manual with the risk of human error ever present.

The rise of ERP and TMS software in the 1980s

ERP and TMS software started to emerge in the 1980s to help businesses digitize complex operations. These on-premise systems were installed locally on company hardware and managed by specialist IT staff, as many are still to this day.

Robotic process automation

In the 1990s, robotic process automation (RPA) technology introduced software robots, or bots, that could emulate human actions inside digital systems. This meant repetitive tasks like data collection and payment processing could now be automated.

Cloud-based platforms emerge in the late 2000s

New cloud services enabled teams to access financial data remotely, improving access to data, simplifying collaboration, and allowing for reduced costs when compared to a locally hosted TMS.

APIs and real-time processing in the 2010s

Starting in the 2010s, new banking APIs provided access to financial data in real time, increasing reporting accuracy compared to manually imported files. The growth of instant payment schemes like Faster Payments in the UK (2008), SEPA Instant Credit Transfer in the EU (2017), and FedNow in the US (2023) is further accelerating the shift away from file transfers and batch-based processing to real-time settlement, enabling new functionality like continuous reconciliation and instant payment confirmation.

The arrival of modern platforms like Atlar

From the late 2010s onwards, a new breed of treasury platform emerged with the ability to connect to all financial providers, old and new, in real time and with zero up-front configuration. Based on modern, cloud-native, and API-first technologies, these platforms are designed to be easier to implement and intuitive to use while offering rich cash management, payments, reporting, and analytics functionality.

Manual processes and spreadsheets

Ideal for: smaller teams without a dedicated treasury management function that need to perform operational treasury tasks with one or two banks.

Manual treasury management is the de facto approach for many non-enterprise businesses. In a recent survey, the Association of Accountants and Financial Professionals found that two-thirds of finance teams still rely heavily on spreadsheets and manual processes.

In practice, this involves a combination of bank portals, spreadsheet reports, and perhaps basic financial management tools. Some banks provide entry-level cash management features, for instance. These setups require multi-step workflows to gather data, transfer files, and create reports: the finance team at Sellpy spent 60 hours every week on manual payments and reporting for a relatively small number of banks.

To make payments, finance teams log into individual bank portals and enter counterparty details manually or upload a file. If a payment requires approval by another team, they’ll need to access the bank portal or log into another system like an ERP. Without a central platform to manage bank access rights and approvals, collaboration happens asynchronously and comes with risks. Reconciliation may need to be done manually by comparing bank statements with internal records line by line.

As for financial reporting, balance and transaction data needs to be downloaded from bank portals, reformatted, and imported into a custom-built spreadsheet in Excel or Google Sheets – unless the data is logged by hand manually. Naturally, these reports are error-prone and static, showing the company’s financials at a point in time. More advanced analysis like cash flow forecasting is unlikely to be attempted to any great extent, due to the difficulty of creating and updating the models manually.

Advantages of manual processes

Low up-front cost

With no lengthy implementation project, manual processes let teams get started quickly with basic treasury management activities. The up-front cost is effectively zero, which can be compelling when judged against the cost of traditional TMS software.

No tech resources needed

Finance teams can be discouraged from implementing a TMS by the need for specialists and IT support, since bank integrations are often managed internally. Spreadsheet programs like Excel present no such problems.

Does the basics well

For companies with straightforward operations and only one or two banks, manual processes can be sufficient to perform basic activities like one-off payments and monthly reporting.

Disadvantages of manual processes

Time-consuming

Manual processes take time and, as a company’s operations become more complex, these processes simply don’t scale. This means more time spent on low-value admin work, possibly the need to hire extra staff, and less time for strategic finance activities.

Prone to error

Human error is all but inevitable with manual workflows, be it a misdirected payment, missing line items, or inaccurate forecasts. This might be stomachable for teams at an early stage but growing companies, those under pressure financially, and those in more regulated industries need 100% accuracy.

Security and compliance risks

Manual processes often necessitates sharing access to systems and storing sensitive information in non-secure environments, and there’s a risk of regulatory noncompliance in the event of errors. This can lead to data breaches, fines, reputation damage, and worse.

ERP treasury modules

Ideal for: businesses with an existing ERP system in place, relatively simple treasury management needs, and some in-house bankconnectivity expertise.

ERP systems like SAP S/4HANA and Oracle’s NetSuite have offered finance tools for decades, from budgeting and invoicing to maintaining a general ledger. Some have started to offer modules with basic treasury management functionality around cash management and payments, stopping short of features like payment automation, advanced forecasting, and automated interest rate and FX riskmanagement.

The main benefit of using ERP treasury modules is that you avoid the cost of implementing another system and, if your ERP is well maintained and integrated with all of your banks, you can harmonize treasury management with the rest of the business using one shared source of information.

In reality, ERPs are not specialized in bank connectivity. To use an ERP for tasks like reconciliation, payment details and bank feeds need to be funneled into the system from the bank. Some ERPs offer out-of-the-box connections to select banks, but generally those connections lack basic functionality such as the ability to pass along full reference and payer details.

When a bank connection is missing or underperforming, one option is for businesses to build it themselves. ERP bank integrations are complex, since the connections were not designed to be interoperable. It requires a specialized, well-staffed IT team to coordinate with the bank for several months while at the mercy of the bank’s own timelines. With no single standard for bank connectivity, the complexity increases with the number of banks. Each bank offers different channels (host-to-host, EBICS, Swift, API) and requires its own connection, data mapping, and maintenance in line with changing requirements.

Because of the lack of reliable out-of-the-box bank connectivity, most teams have to retrieve data manually from each individual bank portal, reformat it file by file, and then upload the files to their ERP. To make payments, the process is reversed by exporting either CSV or payment files from the ERP and uploading them to each relevant bank portal.

ERPs are a viable option for entry-level treasury management tasks if the system is already established internally and connected to the relevant banks. Many teams will nonetheless opt for purpose-built software with reliable ERP syncing as opposed to an ERP treasury module.

Advantages of ERP treasury modules

Pre-integrated

Once the ERP module is configured it’s possible to perform some core treasury management tasks without a long implementation project and at lower cost, provided the ERP is connected to your banks.

Central system

ERPs help unify an organization’s processes. If your ERP is well-established as the single source of financial truth, there are efficiency gains in using it alongside other teams.

Disadvantages of ERP treasury modules

Lack of connectivity

A key downside with ERPs is the lack of native bank connectivity, resulting in a heavy IT burden during integration and for ongoing maintenance. Some businesses may struggle to integrate new banks as they grow, resulting in incomplete coverage and missing data.

Limited functionality

Some ERPs support operational treasury tasks to a degree, but likely fall short for treasury management functions with strategic responsibilities such as forecasting, optimizing liquidity, and managing FX risk.

Low usability

ERPs are built to handle a high volume of data, but not to automate or simplify treasury management, and are often heavily manual to operate. ERP interfaces can also be outdated and require training to use, negatively impacting their adoption company-wide.

Data availability

ERPs typically suffer from low data freshness since financial data is either uploaded manually or received at intervals of up to 48 hours, limiting the timeliness and accuracy of financial reporting.

Treasury management systems (TMS)

Ideal for: enterprise-level finance teams with complex treasury processes, a multitude of banks, and significant internal resources and budget.

Treasury management systems (TMS) like GTreasury, FIS, and Kyriba started appearing in the 1980s and are the first generation of software applications dedicated to treasury management. These systems were built around a file exchange service that allowed businesses to communicate electronically with banks, a major step forward compared to paper-based documents.

The TMS has since developed into a sophisticated system supporting a broad range of treasury management activities. Still built around the same file exchanges, these systems consist of distinct modules configured by dedicated personnel. Many are even still installed on-premise using the customer's servers, and a majority of systems are upgraded on fixed, once-per-year schedules as opposed to continual platform updates.

Implementing a TMS is typically a major investment. The average implementation time is between 4 and 18 months depending on the provider, according to a 2019 Deloitte report. This plus the need for ongoing maintenance and specialist support has meant that TMS software has traditionally only been used by the largest enterprises with complex financial operations.

A TMS can, however, act as the anchor point of a team’s treasury tooling, connecting banks and integrating with ERP systems. From the outset, TMS software was designed to connect to banks through traditional channels and normalize the incoming files. The flip side is that most systems are unable to connect to modern, API-based finance tooling and their reliance on batch-based processing means data cannot be received continuously in real time. Depending on processing rates, the delay can be up to 48 hours, potentially leaving you with outdated, inaccurate reports.

TMS software is generally optimized for configurability over usability. Enterprise-level finance teams will find their TMS can support all but the most advanced treasury operations. Leveraging this functionality, though, may require some manual intervention and improving reporting or changing processes can be painful. Nevertheless, a properly implemented and user-friendly TMS can be a boost to large enterprises with the resources and personnel to make it their own.

Advantages of a TMS

Bank connectivity

TMS bank connectivity is often superior to that of ERPs and other non-specialized tools, in terms of both quality and quantity. Banks can be connected through their standard channels with the various file formats normalized.

Highly configurable

In catering to large enterprises, many TMS providers deliver their systems in a way that allows for highly bespoke implementations, provided resources are available to manage it on an ongoing basis.

Time-saving automation

The TMS was built to help enterprises automate the most cumbersome financial processes, like data collection, reconciliation, and reporting. This is still a core benefit today, even if manual intervention is sometimes needed.

Disadvantages of a TMS

High cost

TMS software comes with a high price tag, including the initial purchase but also long-term maintenance and updates. The ongoing running costs, including time spent by dedicated personnel and consultants, are high and difficult to reduce without replacing the system entirely.

Lack of modern connectivity

The TMS is adept at connecting to traditional banks, but many are unable to integrate with modern API-first platforms – including newer banks like Revolut, PSPs like Adyen or PayPal, spend management platforms like Pleo or Spendesk, and even a traditional bank’s modern API offering. This results in siloed systems, a lack of any real-time data, and an incomplete picture of your finances.

Complexity and user adoption

TMS software can be intricate, unintuitive, and plagued by outdated interfaces. This can lead to slower adoption rates internally and more time and resources devoted to training.

Provider lock-in

The investment required to implement a TMS means that the cost and effort of switching to another system is high. Depending so heavily on a single provider for updates, support, and pricing often leads to less favorable terms over time.

Modern treasury platforms

Ideal for: businesses using several or more banks, with or without a dedicated treasury management function, plus limited budget for tooling and IT support.

For a time, deciding on treasury management tooling was effectively a choice between sticking with manual processes, bank portals, and spreadsheets, or committing to a heavy-duty enterprise system that might take years to provide a clear ROI. In short, a choice between legacy treasury software or none at all.

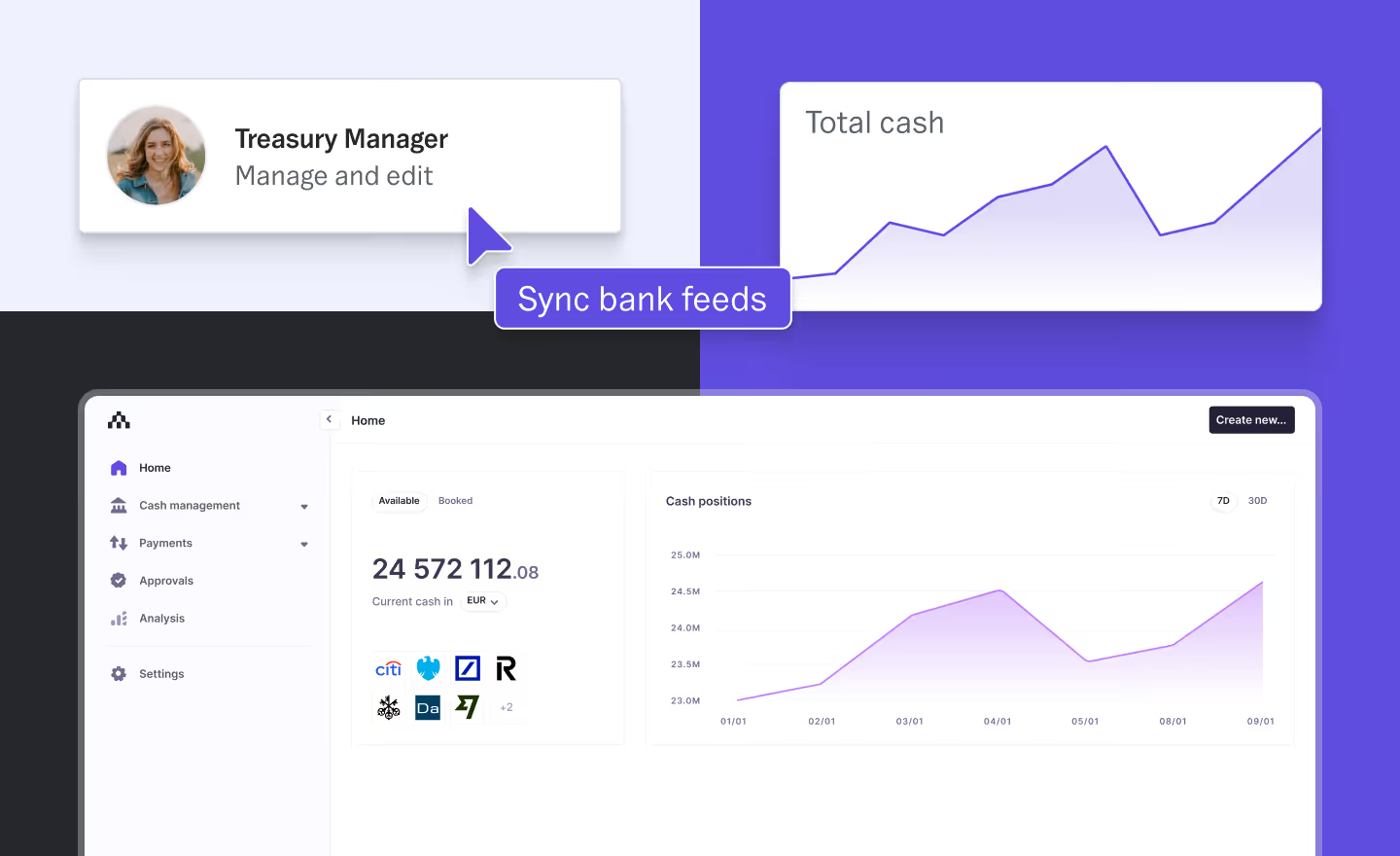

A middle ground is now emerging in the form of modern, real-time, and API-ready platforms like Atlar. These platforms can connect to banks and ERPs using the same channels as a TMS, but are generally built to support real-time integrations with finance tooling of all kinds. Instead of only processing batched files from banks with a delay, most modern platforms can receive data continuously from any provider.

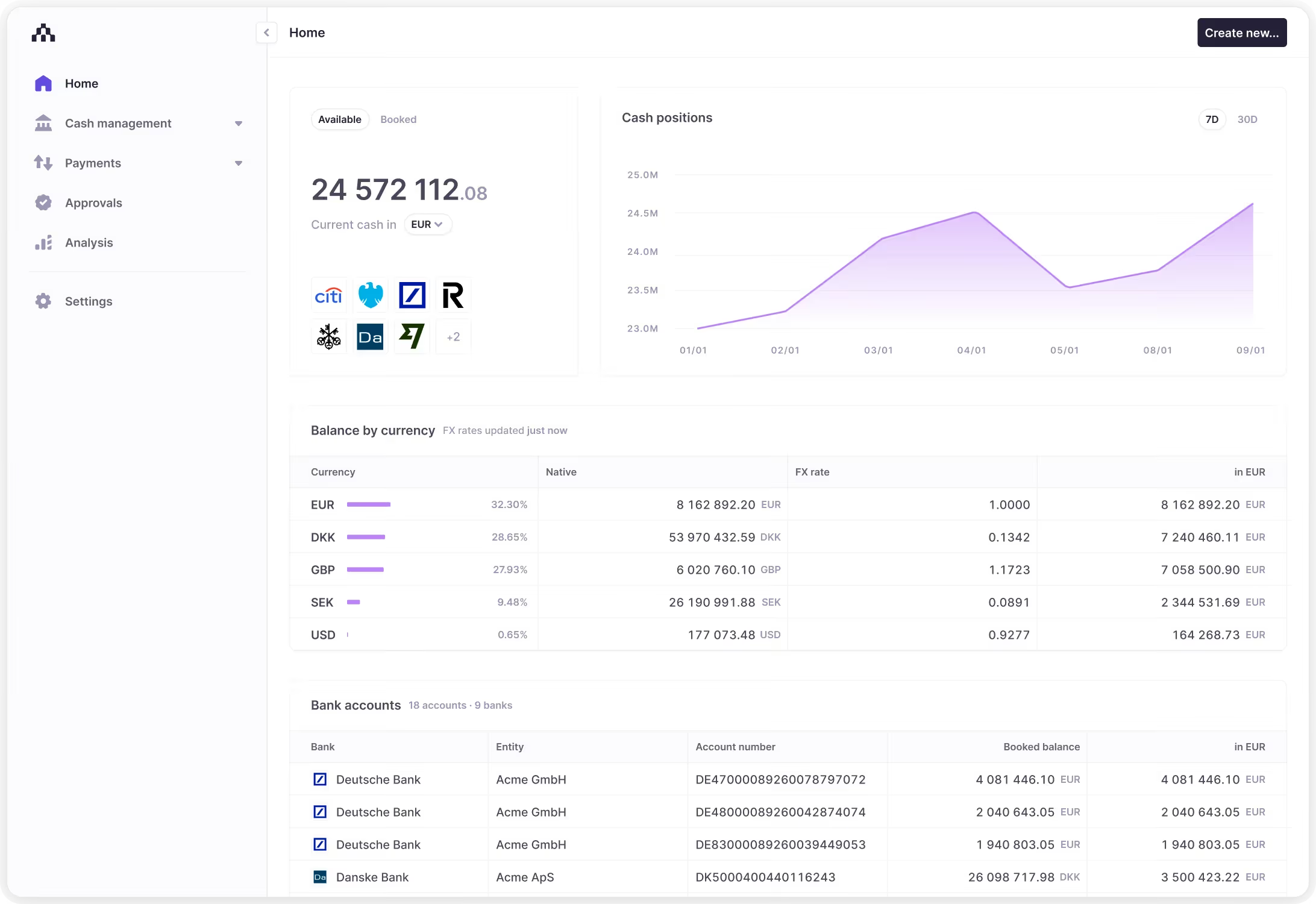

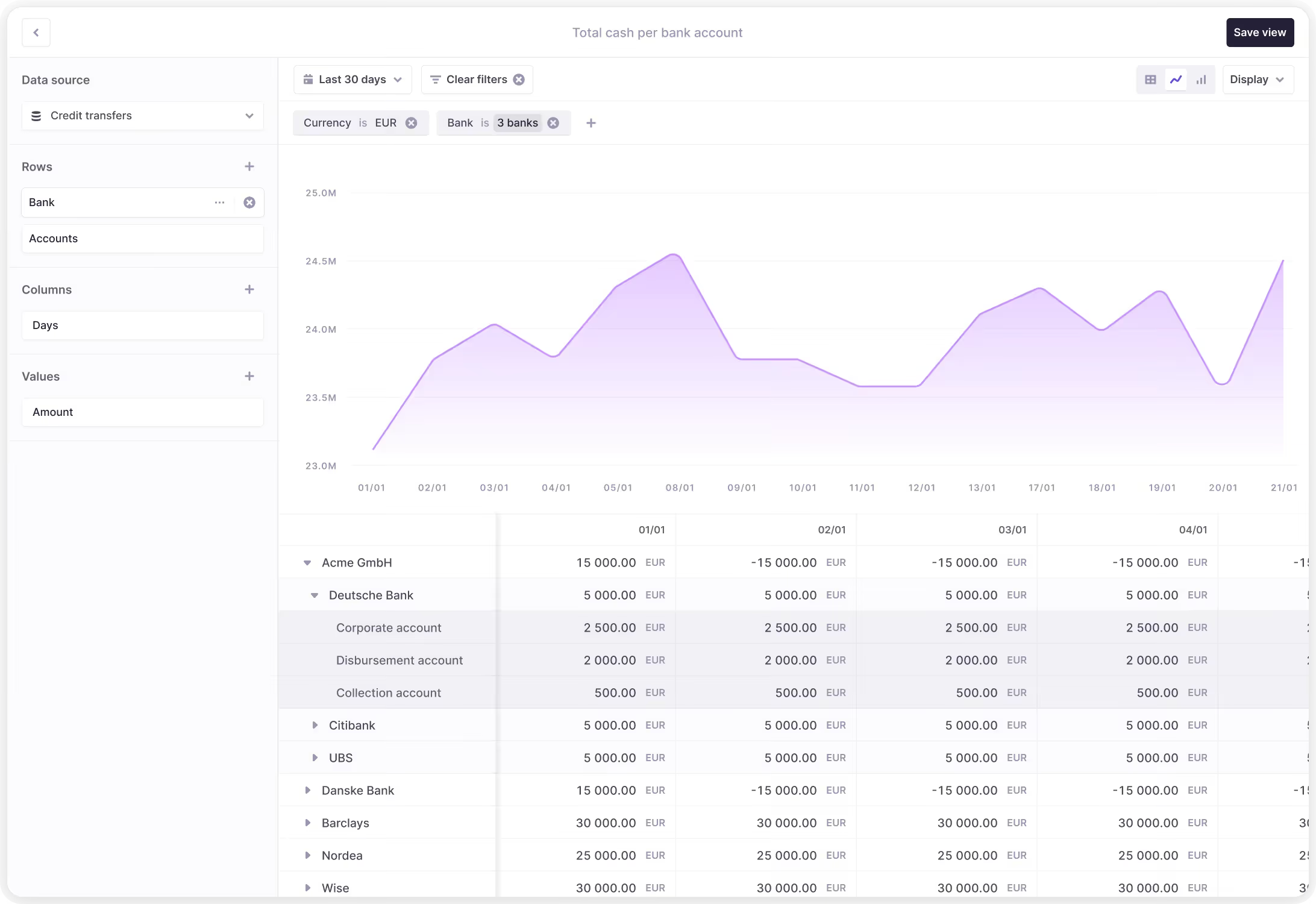

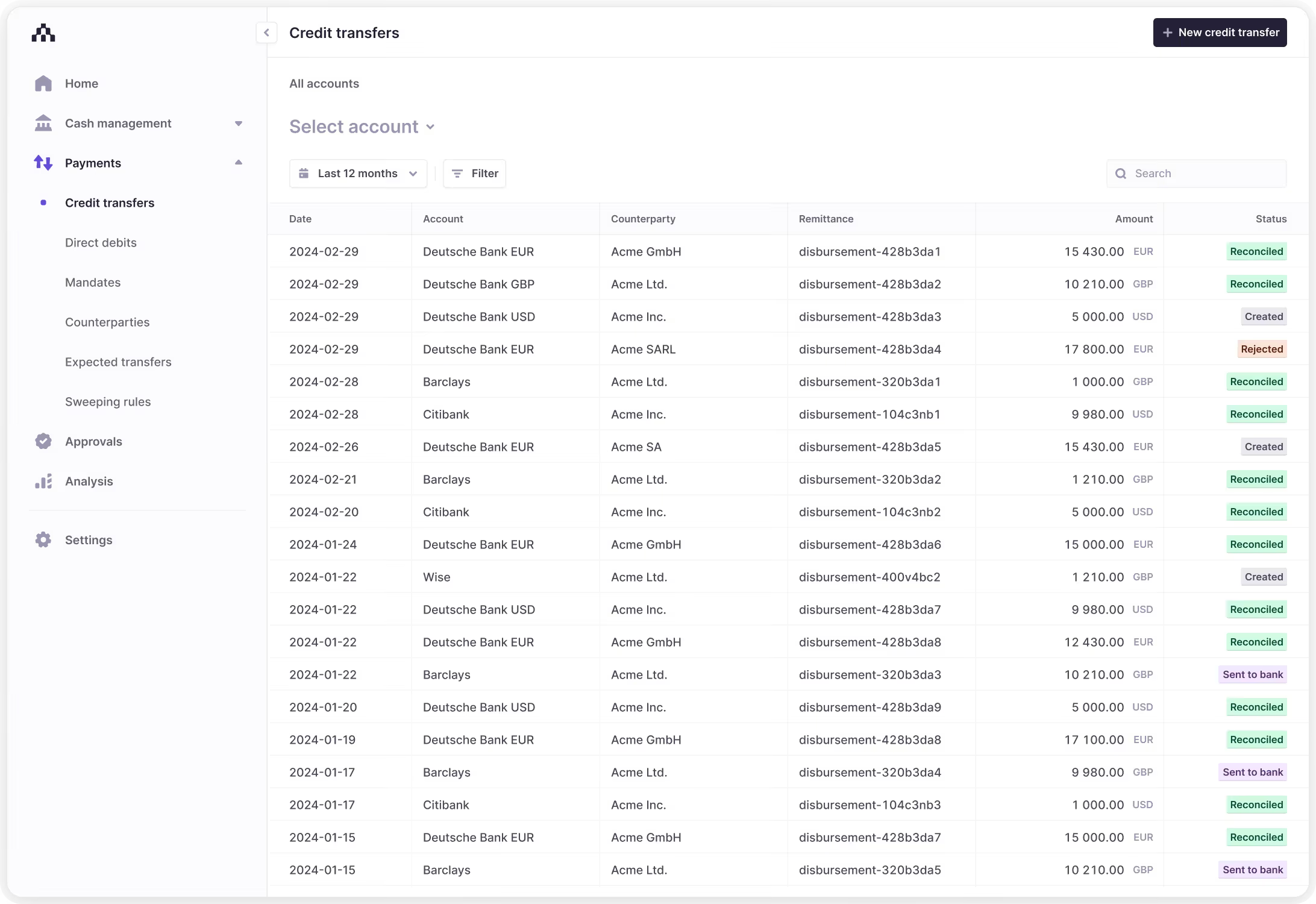

A fundamental benefit of treasury tooling is the ability to centralize financial data and payments in one place, letting teams see their cash positions across multiple bank accounts in one dashboard and make payments without the need for multiple logins. This is true of both a TMS and more modern platforms, and the reduced time spent on admin work is a major advantage for finance teams used to uploading and downloading files on a daily basis.

Unlike manual spreadsheet reporting, modern treasury platforms enable full cash flow visibility at any given time, which makes more strategic decision-making that much easier. And unlike legacy TMS interfaces, these platforms are designed with modern UX principles and ease of use in mind – without compromising on functionality. This helps make more advanced analytics features like forecasting more readily usable, rather than requiring dedicated training or specialist help.

The time and effort required to implement a modern treasury platform is often much lower compared to a TMS, taking a matter of weeks instead of months or years. This lets finance teams reap the benefits of process automation sooner. The team at Loomis Pay was able to consolidate all of its bank accounts in three weeks, for example, saving 120 hours every month. Fast-growing scale-up Sellpy was up and running in four weeks, streamlining its treasury processes to save 60 hours per week.

Based on a SaaS model, most modern platforms are not built to match the bespoke configurability of an on-premise or self-hosted TMS. Cloud-native technology, however, can be updated on a continual basis as opposed to fixed annual cycles. This enables modern treasury platforms to adapt quickly to new technologies, regulation, or suggested improvements instead of a six or twelve month wait.

Once a TMS has been implemented, businesses are unlikely to take a decision to switch systems lightly. At the other end of the spectrum, teams relying on manual processes will find that implementing proper treasury tooling always requires some up-front cost and effort. A new wave of platforms, though, is bringing those costs down and enabling modern finance teams to manage money more efficiently and securely than ever before.

How to pick the right tooling for your business

Key assessment criteria

Choosing the right treasury management tooling starts with understanding the complexity of your financial operations, in-house expertise, and engineering resources. Here are some general guidelines.

Selection checklist

Choosing new tooling can be an important decision with long-term implications. This checklist covers some guiding principles to help you approach the selection process.

- Compare functionality: Start by evaluating what features each solution offers and what is a must-have. There is little value in paying for a bloated set of features that your team will rarely use.

- Evaluate ease of use: New systems can quickly become a liability if your team finds it difficult to use. Prioritize finding a tool with a user-friendly interface, simple workflows, and that’s quick to get up and running.

- Assess integration capabilities: Your goal should be to integrate treasury tooling with existing systems, from banks to PSPs and other finance tools, to create one workflow. Real-time capabilities will make your new setup more future-proof.

- Weigh security measures: Since you’re entrusting the system with financial data, make sure to scrutinize its security features. Look for multi-factor authentication, encryption, and access controls as baseline requirements.

- Make a financial assessment: Consider not only the up-front cost, but also ongoing maintenance, training, and potential updates. Weigh these costs against the expected benefits such as time saved and reduced risk.

- Plan the implementation: Finally, develop an implementation roadmap. This should detail the rollout timeline, the time taken to fully integrate banks and other systems, and the level of effort required from your team.

How Atlar can help

As businesses grow, treasury management quickly shifts from an afterthought to one of the most business-critical activities a finance team needs to perform. Processes become more complex and time-consuming, the financial and reputational risk of errors increases, and strategic decisions need to be taken with a higher degree of confidence.

Most finance teams start to evaluate treasury management tooling at some point along this journey. Some may be tempted to delay a decision due to concerns about the investment of time and effort required, and rightly so, when the only alternative was a twelve-month TMS implementation, dedicated personnel, and neverending maintenance.

Modern tooling like Atlar has changed all this, providing customers like Acne Studios, GetYourGuide, and Forto with a single platform that connects to everywhere and gets you up and running in weeks. Finance teams are now better equipped to do the work that keeps our businesses running, saving hours on admin tasks and managing money more efficiently.

Does your team still rely on manual processes for treasury management? See our demo to learn why modern finance teams shift to Atlar instead.