A Guide to UK Bank Payments

The UK operates its own local, non-SEPA schemes to facilitate bank payments. Incumbent schemes like Bacs make up a big chunk of volumes, though the UK is also pioneering its own real-time payment system while centralising its core infrastructure.

Key facts

- Currency: Pound sterling (£)

- ISO currency code: GBP

- ISO country code: GB

- IBAN example: GB29 MYBK 6026 1431 0379 19

- Key local schemes: Bacs Direct Credit, Bacs Direct Debit, Faster Payments, CHAPS

- Settlement agent: Bank of England

Payment infrastructure

Interbank payments in the UK rely heavily on domestic schemes, unlike many eurozone countries that have replaced their local schemes with SEPA payment schemes. This is because British pound sterling is not supported by the SEPA schemes despite the UK being a participant in SEPA.

In order to use one of the UK’s domestic schemes, payments must be sent in GBP between bank accounts domiciled in the UK. To move money locally businesses will need to open a GBP account with a bank that operates a UK branch. Get in touch here for recommendations and introductions to banking partners.

The UK’s three main local schemes are Bacs (Direct Credit and Direct Debit), CHAPS, and the relative newcomer Faster Payments (FPS). These schemes dictate the transactional capabilities of banks and the main push and pull payment types available, similar to those under SEPA: credit transfers, direct debits, and instant credit transfers respectively. A key recent trend has been the rise of the real-time scheme Faster Payments and the migration of volume away from batch-based systems.

Other parts of this ecosystem have been around for decades: Bacs was introduced in 1968 and CHAPS in 1984. Today each scheme operates based on its own rules and infrastructure, though this is set to change under the New Payments Architecture (NPA). The NPA aims to bring about a once-in-a-generation overhaul of UK interbank payments, centralising the main schemes into a single settlement system over the next decade.

Push-based payments

CHAPS, Bacs Direct Credit, and Faster Payments facilitate push payments and each come with their own distinct fees, settlement time, and use cases. Bacs Direct Credit (a ‘bank transfer’) is used to make regular payments like those for salaries, pensions, and state benefits. It forms part of the UK’s leading payment scheme together with Bacs Direct Debit and processes payments in around three business days.

CHAPS, one of the largest high-value payment systems in the world, is used predominantly for large transactions and corporate treasury. Faster Payments, launched in 2008, is one of the first truly 24/7, 365 days a year real-time payment schemes. Funds appear immediately in the payee’s bank account and payments are free for consumers – but businesses can incur higher costs.

Pull-based payments

Bacs Direct Debit is the UK’s predominant pull payment type and is typically used by consumers to pay for things like recurring bills and subscriptions. In 2022, around 70% of all regular bill payments were made using Direct Debit according to UK Finance. Though well-established among consumers, businesses tend to use it less due to the lack of control over the amount and timing of outgoing payments.

Market data and trends

While Bacs and CHAPS are both relatively stable in terms of usage and track UK economic performance closely, Faster Payments is experiencing remarkable volume growth. In 2021, Faster Payments overtook Bacs Direct Credit as the most popular payment method among businesses to make payments, accounting for 43% of all payments. Volumes have shot up from 614 million payments in 2012 to 4.3 billion in 2022 and grow around 15-20% each year.

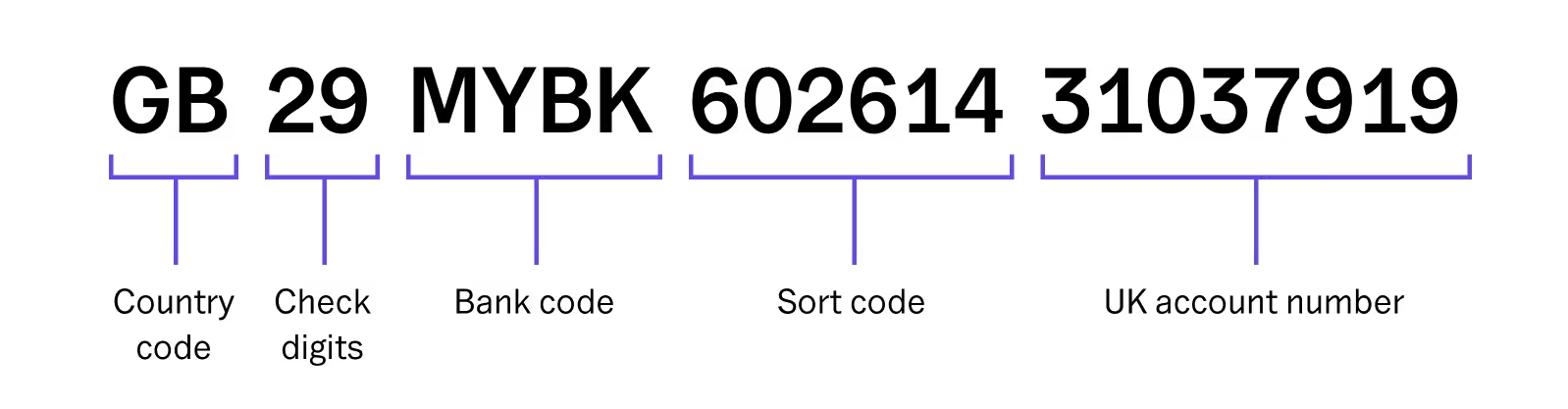

Total transaction value by scheme, 2021-2022

While CHAPS was responsible for only 0.1% of payment volume in 2022 (52 million), it represented 90% of value – totalling £98.6 trillion – showing the extent to which it’s used for financial and corporate treasury purposes.

Looking at Bacs specifically, Direct Debit accounts for 70% of Bacs volume but only roughly 25% of value. This reflects the fact that Direct Credit is typically used for larger payments, like the UK government disbursing state benefits and pensions.

Faster Payments is seeing strong growth in total transaction value processed too, increasing by 25% from 2021 to 2022. Looking ahead, the continued development of the UK’s open banking sector could potentially drive further growth for Faster Payments if it can establish a foothold in retail payments.

Bank account numbers in the UK

- BBAN format: AAAA XXXX XXYY YYYY YY

- IBAN format: GBDD AAAA XXXX XXYY YYYY YY

- Country code: GB

- Check digits (D): 29

- Bank code example (A): MYBK

- Sort code example (X): 60-26-14

- Account number example (Y): 3103 7919

- BBAN example: MYBK 6026 1431 0379 19

- IBAN example: GB29 MYBK 6026 1431 0379 19

The UK’s Basic Bank Account Number (BBAN) – which forms the domestic part of the IBAN – consists of a four-character bank code, a six-digit numeric sort code, and an eight-digit numeric account number.

The sort code is the equivalent of a Bank Identifier Code (BIC) or SWIFT code and is unique to the UK and Ireland. The first two digits of a sort code identify the bank and last four identify the specific branch. The account number refers to a specific bank account and typically contains eight digits, though some UK banks use shorter account numbers and prefix them with the number ‘0’ to reach eight digits. Bank account numbers are generally only used in conjunction with a sort code.

BBANs are formatted as AAAA XXXX XXYY YYYY YY, where A represents the bank code, X denotes the sort code, and Y the account number. The bank code is the first four characters of the bank’s BIC code, which uniquely identifies the institution globally.

For international transactions, the International Bank Account Number (IBAN) is used. UK IBANs include the BBAN plus a four-character header. This header includes 'GB', which stands for the two-letter national bank code from ISO 3166 for the United Kingdom, along with two check digits.

UK IBANs are presented as GBDD AAAA XXXX XXYY YYYY YY where GB is the country code, DD the check digits, followed by the BBAN.

Clearing and settlement

While there are several clearing houses in the UK, the sole settlement agent is the Bank of England, the central bank which also operates CHAPS. This contrasts with the SEPA region throughout which various local and pan-European clearing and settlement mechanisms (CSMs) operate.

The infrastructure that underpins settlement of sterling payments is the Bank of England’s real-time gross settlement (RTGS). It holds balances in accounts for institutions like banks and building societies and transfers funds in real time between account holders, ensuring risk-free, final, and irrevocable settlement.

Alongside implementing the NPA to centralise the UK’s various schemes and better support real-time payments, the Bank of England is also upgrading its RTGS service by 2025 to meet ISO 200022 standards.

Payment methods

Bacs Direct Credit

- Year introduced: 1968

- Operated by: Bacs (now part of Pay.UK)

- Maximum amount: £20 million per payment (may vary by bank)

- Availability: Monday to Friday between 07.00 and 22.30

- Settlement: Up to three business days

- Fee per payment: 1.85 kr. (approx.)

Bacs Direct Credit allows businesses of any size to make payments directly into the accounts of another bank or payment service providers (PSPs) with a three-day settlement period. Around 8 in 10 Brits have their salaries paid through Direct Credit and it’s the most common payment method for regular payments.

Compared to handling paper money like cash and cheques, Bacs Direct Credit is much easier for businesses to manage. Remittance and reconciliation can be automated, there are fewer security requirements, and the regular settlement cycle simplifies cash flow forecasting to some extent.

Credit transfers through Direct Credit can be submitted up to 30 days in advance of the desired payment date, making it well-suited for regular, scheduled payments like salaries. Payments can also be recalled after submission if the bank or PSP is notified before the cut-off time.

Processing cycle

- Day 1: Payment files are transmitted to Bacs between 07.00 and 22.30

- Day 2: The files are delivered to the recipient's bank for processing

- Day 3: The funds are credited to the recipients' accounts and debited from the payer's account

Pros and cons

- Pros: Bacs Direct Credit is available to any business with a UK bank account. It is relatively easy to administer since both remittance and reconciliation can be automated, an offers a comparatively low fee per payment.

- Cons: Bacs Direct Credit is not suitable for immediate or same-day payments due to the three-day settlement period with strict cut-off times. As a push-based payment method, it relies on the payer taking action (unlike Bacs Direct Debit).

Faster Payments

- Year introduced: 2008

- Operated by: Pay.UK

- Maximum amount: £1 million per payment (may vary by bank)

- Availability: 24/7, 365 days a year

- Settlement: Near-instant

- Fee per payment: Typically free for consumers, £0.50+ for businesses

Faster Payments (or FPS), introduced in 2008, is arguably one of the most successful attempts to offer real-time payments at scale. It offers major gains in speed and convenience compared to traditional bank transfer methods. It’s designed to be genuinely real time and operates 24/7, 365 days a year.

As long as both the sending and receiving banks are direct FPS participants, transfer time is typically instant. However, real-time settlement is not guaranteed and it can take up to 2 hours in rare cases. This is because FPS ultimately relies on a deferred net settlement model with a maximum 2-hour cycle, unlike SEPA Instant Credit Transfer (SCT Inst) which has a maximum execution time of 10 seconds.

FPS facilitates real-time payments primarily through online and mobile banking up to a maximum amount of £1 million (this limit can vary from bank to bank). It’s available to anyone in the UK with a bank account, all major UK banks participate in the scheme, and it’s readily accessible through a broad network of traditional banks, fintech firms, and other PSPs that connect either directly or indirectly to the central infrastructure.

Due to the real-time nature of Faster Payments, once a payment is sent it cannot be cancelled. However, banks and building societies nevertheless adhere to the industry-wide Credit Payment Recovery process which provides support when a payment is sent in error.

Pros and cons

- Pros: Faster Payments is the quickest way to send and receive payments in the UK, is available 24/7, and offers relatively low fees compared to card-based payment methods. It also boasts increased security with transactions protected by encryption and two-factor authentication.

- Cons: The limit of £1 million per transaction means that Faster Payments is unsuitable for some B2B use cases, and not all UK banks are direct participants of the scheme.

CHAPS

- Year introduced: 1984

- Operated by: Bank of England

- Maximum amount: No upper limit per payment (may vary by bank)

- Availability: Monday to Friday between 06.00 and 18.00

- Settlement: Same-day if submitted before 17.40 (may vary by bank)

- Fee per payment: £20+

CHAPS is a same-day sterling payment system specialising in high-value payments and is one of the most heavily used schemes of its kind globally. Run by the Bank of England, it guarantees risk-free settlement and irreversible transactions for around 30 direct participants, namely large banks and payment providers. Businesses that use CHAPS access it exclusively through their banking partners, as opposed to participating in the scheme directly.

There’s no transaction amount limit for CHAPS payments and they’re typically used for larger financial transactions, such as settling money market and foreign exchange transactions, corporate payments to suppliers, and one-off purchases like cars or houses.

The scheme is available on weekdays from 6 AM with participant banks required to begin receiving payments by 8 AM. It closes at 6 PM for interbank transactions, while consumer payments must be submitted before 5:40 PM at the latest or they’ll settle on the next business day (some banks impose their own earlier cut-off time).

CHAPS leverages the Bank of England's real-time gross settlement (RTGS) infrastructure and the SWIFT messaging network to maintain high availability and reliability.

Pros and cons

- Pros: CHAPS offers a same-day settlement guarantee, provided the payment is sent before the cut-off time, and there's no transaction amount limit.

- Cons: CHAPS charges significantly higher fees relative to other schemes (around £25 on average) and it is difficult if not impossible to cancel a payment once it has been made.

Bacs Direct Debit

- Year introduced: 1968

- Operated by: Bacs (now part of Pay.UK)

- Maximum amount: £250,000 per payment (may vary by bank)

- Availability: Monday to Friday between 07.00 and 22.30

- Settlement: Up to three business days

- Fee per payment: £0.05-0.50

The concept of a direct debit originated in the UK in the 1960s and today Bacs Direct Debit is by far the most common way to pay on a recurring basis. A Direct Debit is an instruction from a customer to their bank that authorises an organisation to collect payments directly from the customers' bank account.

This instruction takes the form of a Direct Debit mandate, which provides advance notice of the payment amounts and dates and can be completed via a paper form or online.

Bacs Direct Debit is typically used for things like regular bill payments and subscriptions but can also be used for invoices and ad hoc, one-off payments. Though the Bacs processing cycle of three business days makes it unsuitable for payments requiring same-day settlement, as in most retail and ecommerce use cases.

If the amount, date, or frequency of a Direct Debit are to ever change, the organisation usually has to notify the customer at least 10 business days in advance. And if a payment is made erroneously, the customer is entitled to a full and immediate refund under the Direct Debit Guarantee.

Customers can also cancel a Direct Debit any time, typically by contacting their bank or building society.

Processing cycle

- Day 1: Payment files are transmitted to Bacs between 07.00 and 22.30

- Day 2: The files are delivered to the recipient's bank for processing

- Day 3: The funds are credited to the recipients' accounts and debited from the payer's account

Pros and cons

- Pros: Bacs Direct Debit is available to any business with a UK bank account and provides a low-maintenance and long-lasting recurring payment mandate.

- Cons: Bacs Direct Debit is not suitable for immediate or same-day payments due to the three-day settlement period. If the payer’s bank account does not have sufficient funds, the sending bank may refuse to pay the direct debit.

Looking ahead

The shift to real time

The UK is investing heavily in its real-time infrastructure. In fact, one of the core aims of the NPA is to enable more real-time payments and slowly deprecate the traditional three-day processing cycle associated with Bacs. The shift away from batch-based payments comes with major implications for businesses and platforms relying on manual workflows and legacy infrastructure.

Real-time, 24/7 settlement means payments will be initiated and received continuously regardless of whether it's after 5 PM, over a weekend, or during a holiday. Continuous settlement will require greater automation of both initiation and reconciliation, live status tracking, and new workflows like automated retries and faster approvals.

The Atlar platform is built to support real-time payment flows in the UK and elsewhere out of the box. To hear how we can help set your team up for real time, get in touch with us here.

Variable Recurring Payments

Next to the NPA and the rise of Faster Payments, the emergence of Variable Recurring Payments (VRPs) is potentially one of the most important developments in UK bank payments in recent years.

VRPs are a type of open banking API that enable recurring payments similar to a direct debit, except the amount and frequency can vary without the account holder having to reauthorise and settlement would take place in real time. One use case could be paying a variable amount for your electricity bill based on your actual consumption via a smart meter.

In 2021, the UK’s Competition and Markets Authority (CMA) ruled in favour of the UK’s open banking implementation body by mandating VRPs for sweeping services (or me-to-me payments) between bank accounts held under the same name. Since then the UK’s largest banks have built their own APIs to enable sweeping VRPs. To date there’s no equivalent mandate covering VRPs for commercial use cases, like the paying of bills.

If commercial VRPs are fully adopted by UK banks, they will entail lower transaction costs for businesses relative to card payments while offering more control than direct debits. For consumers they should provide a means to safer, more flexible recurring payments without needing to manually fill in any forms.

How Atlar can help

With Atlar, you can access local UK payment schemes through a single API while continuing to use your existing banks. You can automate both credit transfers and direct debits from initiation to reconciliation, with support for Faster Payments and real-time settlement built-in.

Returns are also handled automatically, and consolidated data from all your banks is available in the Atlar dashboard or via API so you can monitor transactions and balances in real time.

This potentially saves tons of hours that would otherwise be spent manually initiating and tracking payments, not to mention the resources required to build and maintain direct integrations with UK banks.

From the migration to real time to potential scheme changes under the NPA, UK bank payments will continue evolving. Atlar’s payment and treasury automation platform makes adapting to infrastructure changes quick and painless, now and in the future.

Get in touch

If you're a company looking to more easily manage cash at UK banks or automate payments over UK schemes, we'd love to speak with you. Book a demo here.