Bank Account Management in Atlar: FBAR Reporting and Signatory Tracking

Your treasury platform knows your bank accounts. It holds the balances, processes the transactions, and connects to the banks. But ask anything beyond that, and most platforms go quiet. Which entity owns each account? What's the institution's mailing address? Who is authorized to operate it?

These are the questions that surface every year when FBAR filing season arrives (the deadline for tax year 2025 is April 15, 2026), every time someone leaves the company and you need to revoke their signatory access, and during any audit where knowing what you hold at each bank matters as much as knowing what you moved through it. The reason they're hard to answer isn't complexity. It's fragmentation: data split across bank portals, spreadsheets, and systems that don't talk to each other.

We built both FBAR reporting and signatory tracking into Atlar, as part of our Bank Account Management feature set, because the data they depend on is already in the platform. Here's how each works.

FBAR reporting

The Foreign Bank Account Report (FinCEN Form 114) requires US persons, including corporations and LLCs, to report every foreign financial account if the aggregate maximum value exceeds $10,000 at any point during the calendar year. Penalties can reach $16,536 per non-willful violation and significantly more for willful ones. The data required per account is straightforward: institution name and address, account number, account type, currency, owning entity, and maximum value during the year in USD. The pain is in assembling it.

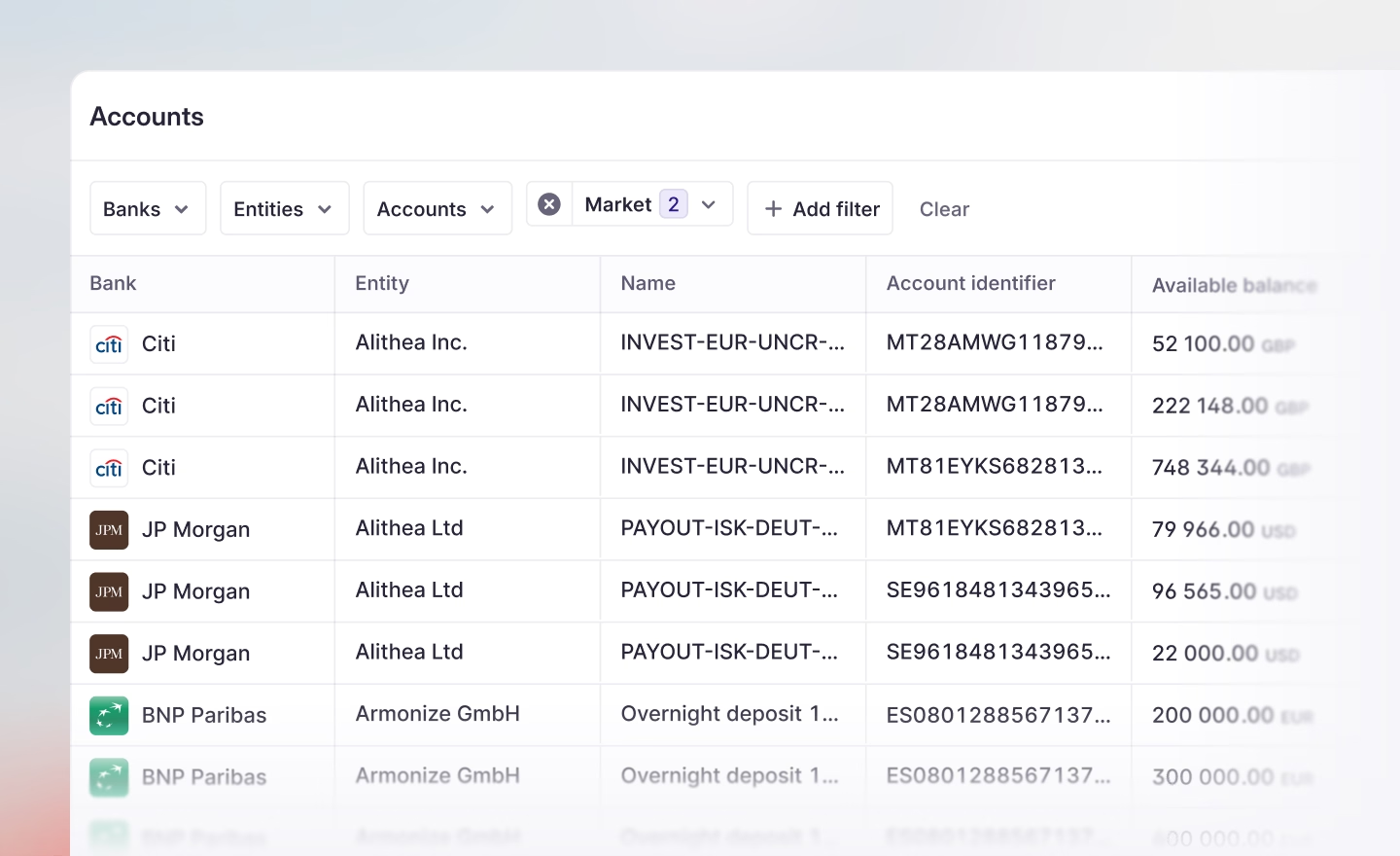

Because your accounts, balances, institution details, and entity mappings already live in Atlar through your bank connections, the FBAR report pulls this together in the structure FinCEN 114 requires. Atlar integrates with banks in over 100 countries, and teams at companies like Lovable, Flex, TradingView, and Babbel already manage their full account inventory on the platform. Each account is flagged if it exceeds the $10,000 threshold, and the report can be filtered by year and exported as a CSV for your compliance team to transfer into the FinCEN 114 form.

Parts of the process remain outside the platform: FX conversions should use the official Treasury Department year-end rate, most organizations will want advisors to review the output, and the submission itself goes through FinCEN's BSA E-Filing System. But the data preparation, which is where the weeks go, is done.

Signatory tracking

In our conversations with US treasury teams, signatory management comes up just as often as FBAR, but as a different kind of problem: persistent and operational rather than annual and compliance-driven.

For every bank account your organization holds, someone needs to know who is authorized to operate it and when that last changed. At scale, this is hard to maintain. People join, leave, or change roles. Banks each have their own processes for updating signers. The information that matters, who can actually move money today, ends up scattered across bank portals, board resolutions, and spreadsheets that go stale quickly.

What treasury teams want is a single view: every account, its current authorized signatories, and when they were added. When someone leaves, you should be able to see every account they have access to and act from one place.

Atlar now provides per-account signatory tracking alongside the FBAR report. For each account, you can record authorized signatories and their roles. Having this data in the same platform where you manage everything else about those accounts is a real step up from a standalone spreadsheet. Over time, we plan to build on this with change tracking, approval workflows, and periodic attestation.

The compliance case for connectivity

FBAR reporting and signatory tracking are more connected than they first appear. FinCEN 114 requires reporting not only on accounts your organization owns, but also on accounts where individuals have signature authority. Knowing who can operate which account isn't just an operational concern; it's a regulatory one.

Both workflows depend on structured data about your bank accounts that goes beyond balances and transactions, and both are painful because that data is fragmented. If your platform connects to your banks, holds your full account inventory, and maps accounts to legal entities, these become natural outputs rather than standalone projects.

This is an overlooked benefit of deep bank connectivity. It's usually framed in terms of cash visibility, payments, or reconciliation. The compliance payoff gets less attention, but it's real: when the data is already consolidated, the reports that depend on it stop being multi-week exercises.

Both features are live now. If you'd like to see how they work with your account structure, get in touch or book a demo.