A Guide to Debt Management for Finance and Treasury Teams

Corporate debt is among the most useful tools a company has, but only when it is managed well. Whether you are tracking external bank loans and credit facilities or managing intercompany lending across subsidiaries, good debt management protects liquidity, controls costs, and supports growth. This guide covers what finance and treasury teams need to know about both external and internal (intercompany) debt: the core processes, the common pitfalls, and the practices that keep you in control.

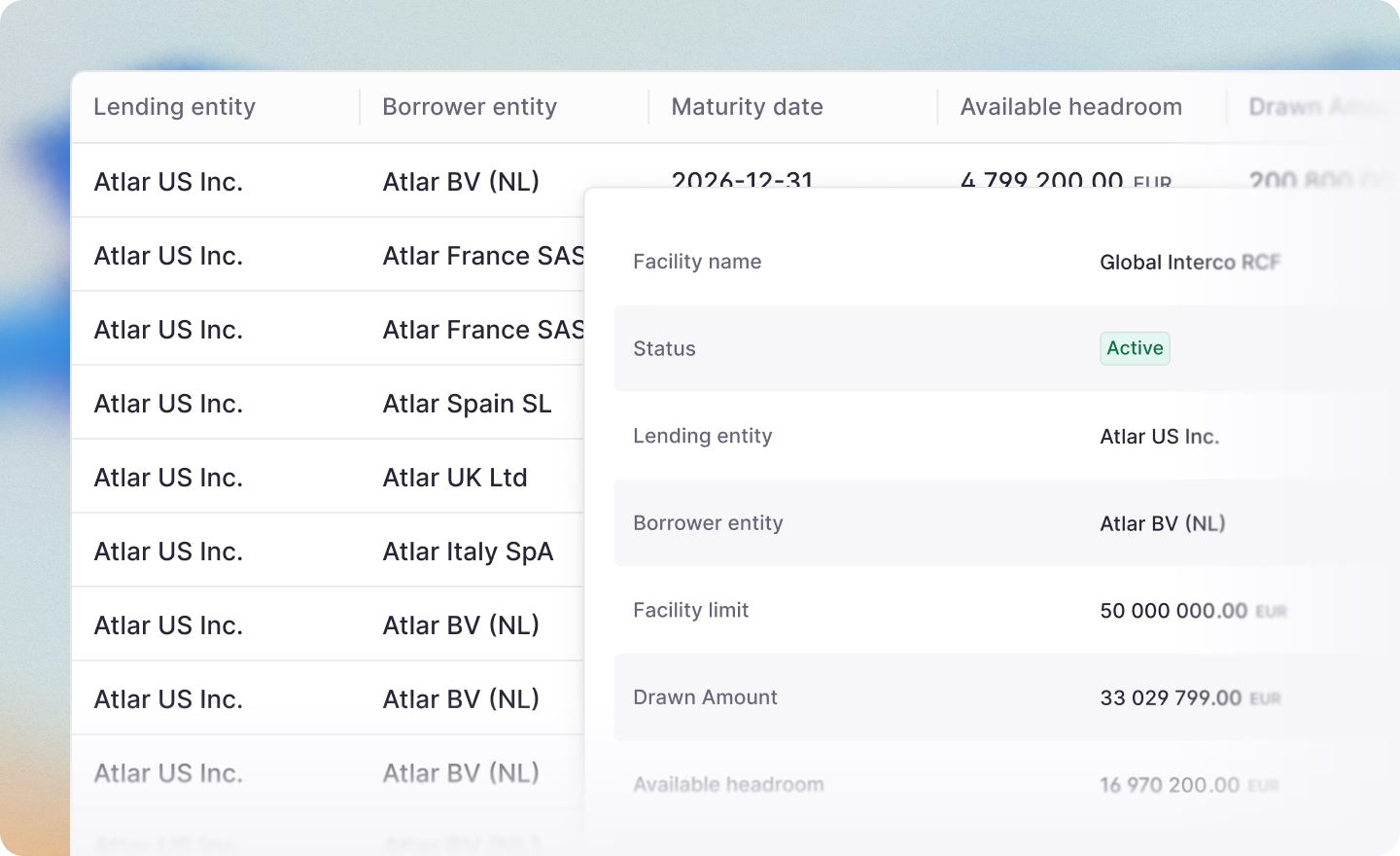

Atlar’s debt management capabilities, currently in beta, enable finance teams to register and track all types of corporate debt—from bank loans and bonds to intercompany loans—alongside their cash positions, payments, and forecasts. To learn more, get in touch with our team.

What is corporate debt management?

Corporate debt management is the process of tracking, organizing, and optimizing a company's borrowing across all debt instruments and entities. It encompasses everything from recording loan terms and monitoring repayment schedules to calculating interest obligations and assessing the impact of debt on cash flow.

For finance and treasury teams, debt management sits at the intersection of several core functions: cash management, cash flow forecasting, financial reporting, and risk management. The debt a company carries directly affects its liquidity position, its ability to invest, and its obligations to lenders and other stakeholders.

In practice, corporate debt falls into two broad categories:

- External debt: Borrowing from banks, bondholders, and other third-party lenders. This includes term loans, revolving credit facilities, bonds, and other credit instruments.

- Internal (intercompany) debt: Loans between entities within the same corporate group. For example, a parent company lending to a subsidiary, or one subsidiary lending to another.

Both types require careful tracking, documentation, and management, but they come with distinct challenges. External debt is governed by covenants and banking relationships. Internal debt is governed by transfer pricing rules, tax regulations, and the need for arm's-length terms. This guide covers both in depth.

Why debt management matters

Debt is a fact of life for most companies of any size. How a company manages it shapes its liquidity, its borrowing costs, and its standing with lenders and investors.

Cash flow visibility

Debt repayments, both principal and interest, are among the largest and most predictable cash outflows a company faces. Without a clear picture of upcoming obligations across all loans and entities, treasury teams risk cash shortfalls, missed payments, or inefficient allocation of surplus cash. Integrating debt data into your cash flow forecasting process is essential for accurate liquidity planning.

Cost optimization

The cost of debt is not fixed. Interest rates fluctuate, hedging instruments expire, and refinancing opportunities arise. Finance teams that actively monitor their debt portfolio can identify opportunities to reduce borrowing costs, whether by refinancing at a lower rate, restructuring repayment schedules, or paying down high-cost debt with surplus cash.

Covenant compliance

Most external debt comes with financial covenants—conditions the borrower must meet, such as maintaining certain leverage ratios or minimum cash balances. Breaching a covenant can trigger penalties, accelerated repayment, or even default. Proactive monitoring ensures you stay within limits and can act before issues arise.

Regulatory and tax compliance

Intercompany loans, in particular, are subject to scrutiny from tax authorities. Transfer pricing regulations require that intercompany lending be conducted at arm's length, that is, the interest rate, repayment schedule, and other terms must reflect what unrelated parties would agree to in comparable circumstances. Failure to comply can result in significant tax adjustments and penalties.

Financial reporting and audit readiness

Accurate debt records are a prerequisite for reliable financial reporting under standards like IFRS and GAAP. Auditors review loan documentation, interest calculations, and repayment histories. Maintaining a centralized record of all debt instruments streamlines the audit process and reduces the risk of misstatements.

Types of corporate debt

Before diving into management practices, it helps to understand the main types of debt that finance and treasury teams typically deal with.

Fixed-rate vs. variable-rate debt

A key distinction in any debt portfolio is between fixed-rate and variable-rate (also called floating-rate) instruments.

Fixed-rate debt carries a set interest rate for the life of the loan, providing cost certainty. The borrower knows exactly what each interest payment will be, which simplifies cash flow forecasting.

Variable-rate debt is tied to a benchmark rate plus a margin (or spread). The benchmark rate is a reference interest rate published by a central authority or derived from market transactions. The most widely used benchmarks in corporate lending are:

- EURIBOR (Euro Interbank Offered Rate): The benchmark for euro-denominated loans. EURIBOR is published daily across five maturities (one week, one month, three months, six months, and twelve months) by the European Money Markets Institute (EMMI). It represents the average rate at which a panel of major European banks lend to each other in euros. The three-month and six-month EURIBOR rates are the most commonly used in corporate loan agreements.

- SOFR (Secured Overnight Financing Rate): The primary benchmark for US dollar-denominated loans, replacing the now-discontinued LIBOR. SOFR is published by the Federal Reserve Bank of New York and is based on actual overnight repurchase agreement (repo) transactions backed by US Treasury securities.

- SONIA (Sterling Overnight Index Average): The benchmark for British pound-denominated loans, administered by the Bank of England. It reflects the average interest rate at which banks lend to each other overnight in sterling.

The interest cost on a variable-rate loan fluctuates as the benchmark rate changes. For example, a loan priced at three-month EURIBOR + 2.00% will see its interest rate reset every three months based on the prevailing EURIBOR rate. If the three-month EURIBOR is 2.50%, the all-in rate is 4.50%. If EURIBOR moves to 3.00% at the next reset, the all-in rate becomes 5.00%.

Many companies hold a mix of fixed and variable-rate debt. The balance between the two, and the use of hedging instruments to manage rate exposure, is a fundamental decision in debt management.

Hedging instruments

Companies with variable-rate debt often use hedging instruments to protect against adverse interest rate movements. The most common types are:

- Interest rate swaps: A contract between two parties to exchange interest payment streams. In a typical "pay-fixed, receive-floating" swap, the company pays a fixed rate and receives a floating rate (e.g., EURIBOR), effectively converting its variable-rate loan into a synthetic fixed-rate obligation. Swaps are the most widely used interest rate derivative in corporate treasury.

- Interest rate caps: A contract that sets a maximum (ceiling) on the variable rate the borrower will pay. If the benchmark rate exceeds the cap rate, the cap provider compensates the borrower for the difference. Caps involve an upfront premium but allow the borrower to benefit if rates stay below the cap level.

- Interest rate floors: The inverse of a cap—a contract setting a minimum rate. Floors are more commonly used by lenders than borrowers, but they sometimes appear in structured financing arrangements.

Tracking hedging instruments alongside the underlying debt they relate to is important for accurate interest expense forecasting, hedge accounting under IFRS 9 or ASC 815 (US GAAP), and understanding the company's true interest rate exposure.

Managing external debt

External debt management means keeping full visibility and control over your borrowing from banks, bondholders, and other third-party lenders. For companies with several banking relationships, entities, and currencies, that is both operationally demanding and strategically important.

Step 1: Assess financing needs and select instruments

Effective debt management begins before the first loan is drawn. Treasury teams work with the CFO, FP&A, and sometimes external advisors to determine how much capital the company needs, for what purpose, and over what time horizon. These inputs drive the choice of instrument.

Key considerations at this stage include:

- Purpose and tenor: A short-term working capital need might be served by drawing on a revolving credit facility, while a multi-year capital expenditure program might warrant a term loan or bond issuance.

- Cost of capital: Compare all-in costs across instrument types, including interest rate, fees (arrangement fees, commitment fees, agency fees), and any associated hedging costs.

- Fixed vs. variable rate: Assess the current interest rate environment and the company's appetite for rate risk. In a rising rate environment, locking in a fixed rate may be preferable; in a declining rate environment, variable-rate debt may be cheaper.

- Currency: If the borrowing currency differs from the company's functional currency, the resulting FX exposure must be considered and potentially hedged.

- Lender diversification: Spreading borrowing across multiple banks and instrument types reduces concentration risk.

- Covenants and flexibility: Understand the financial covenants, reporting requirements, and restrictive conditions that each lender will impose. Negotiate terms that provide sufficient headroom for the business to operate.

Step 2: Negotiate terms and execute documentation

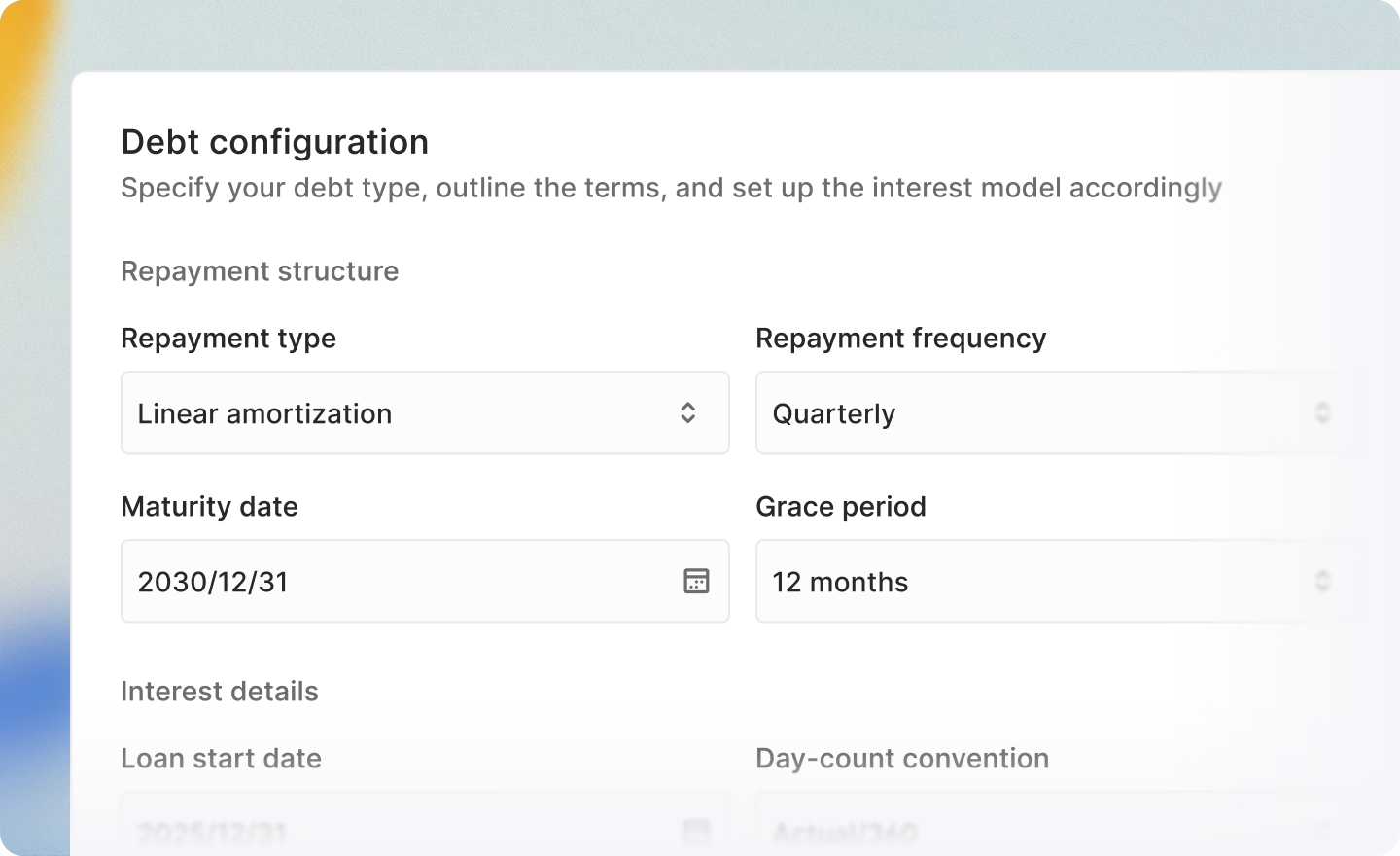

Once the instrument type is selected and lenders are identified, the terms are negotiated and formalized in legal documentation. For a bank loan, this typically includes a loan agreement (or credit agreement) and any related security documents. For a bond, it involves an indenture (the legal contract between the issuer and a trustee who represents bondholders) and an offering memorandum (the disclosure document provided to prospective investors).

Key terms to document and track include:

- Borrower and lender details

- Loan amount, currency, and drawdown mechanics

- Interest rate (fixed or variable, benchmark, margin, reset frequency)

- Repayment schedule (amortizing, bullet, or a combination)

- Maturity date and any extension options

- Financial covenants (leverage, interest coverage, minimum liquidity, etc.)

- Reporting obligations (frequency, format, and content of compliance certificates)

- Events of default and cross-default provisions

- Prepayment terms and any associated fees

- Security or collateral arrangements

This documentation is the single source of truth for each debt instrument and should be stored centrally where the treasury and finance team can access it.

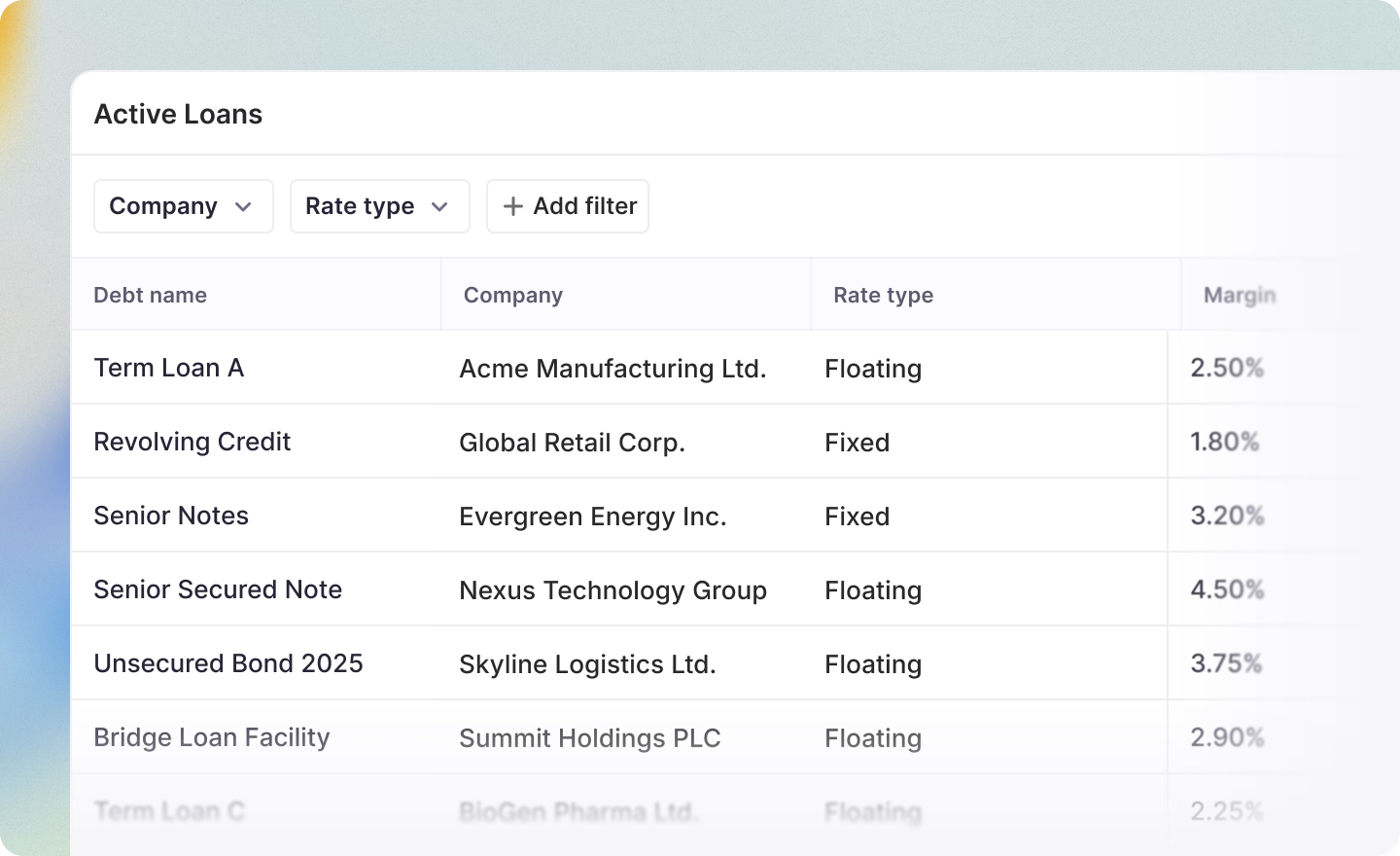

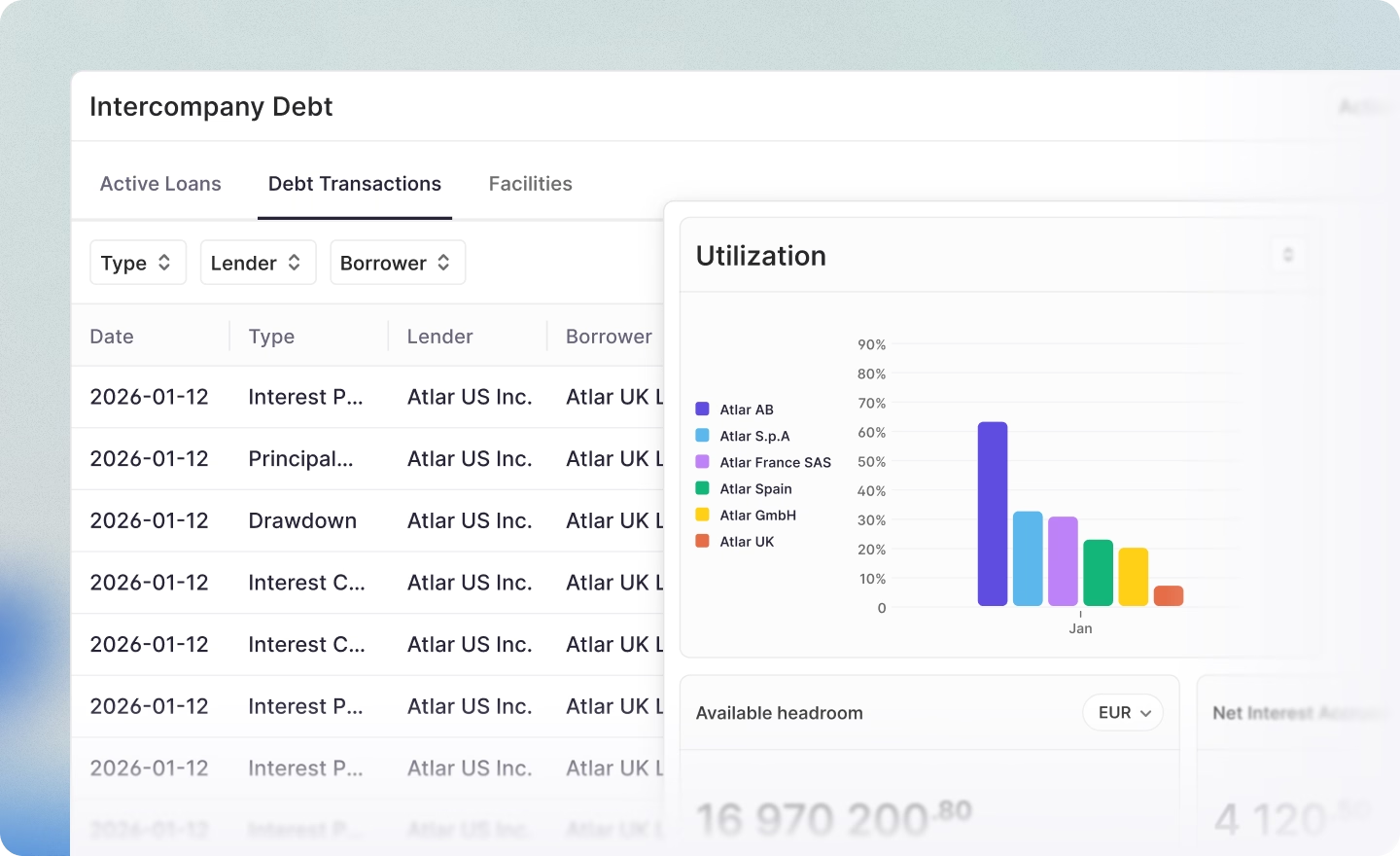

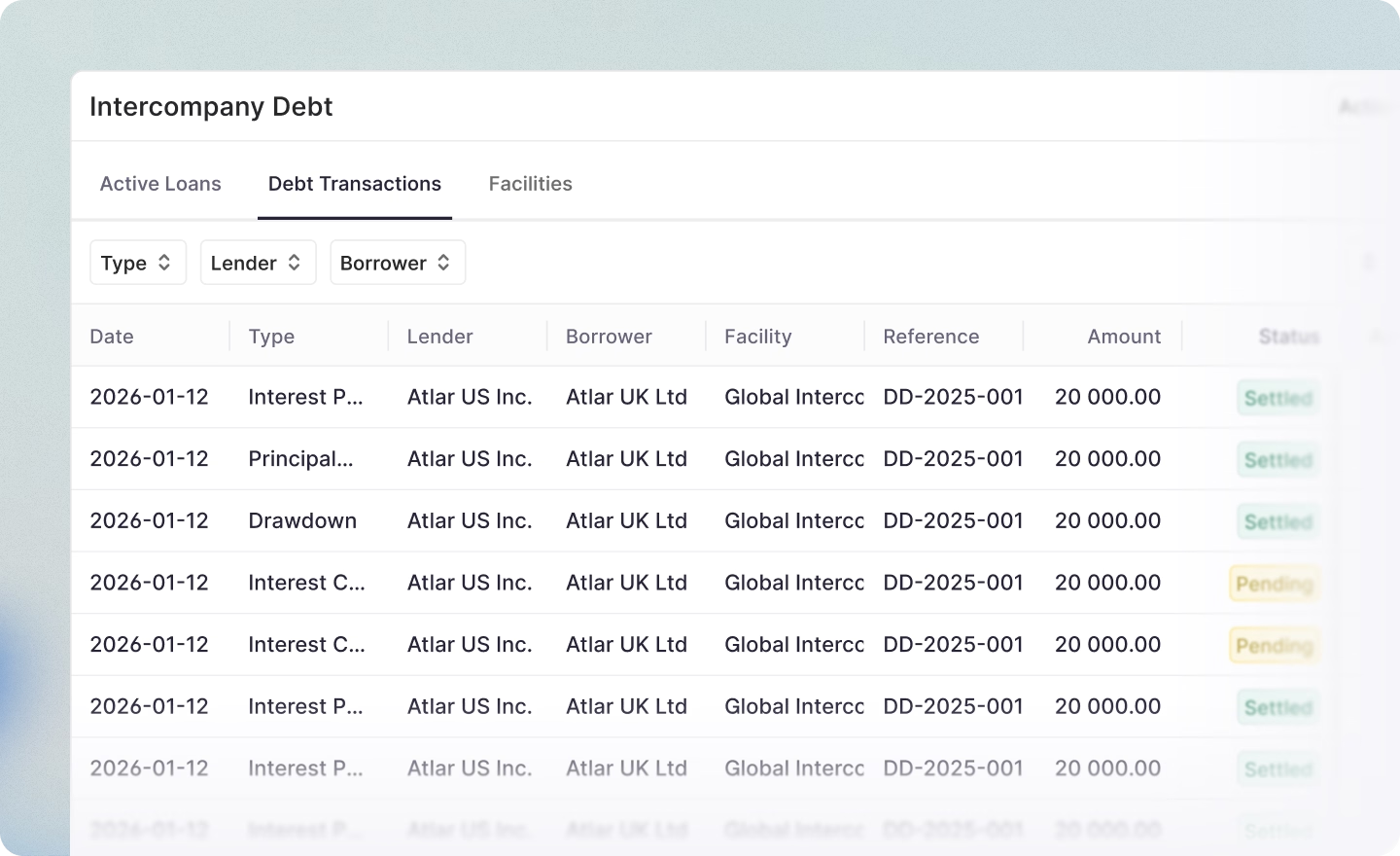

Step 3: Register all loans in a centralized system

With documentation in place, the next step is to register every loan in a centralized debt register—whether that's a dedicated module within a treasury management system (TMS), an ERP system, or (for smaller portfolios) a well-structured spreadsheet. Without this, companies that borrow from multiple banks often end up managing each relationship through separate portals, each with its own statement formats and reporting cycles, making it difficult to assemble a consolidated view of total debt and upcoming obligations. A centralized register with multi-bank connectivity eliminates this fragmentation.

For each instrument, the register should capture:

- Lender, debt type, original principal, and outstanding balance

- Currency and any associated FX hedging

- Rate type, benchmark, margin, and current all-in rate

- Repayment schedule with individual payment dates and amounts

- Maturity date and any bullet or balloon repayment at maturity

- Associated hedging instruments (swaps, caps)

- Covenant thresholds and current metric values

- Links to supporting documentation

This register becomes the foundation for everything that follows: interest calculations, cash flow forecasting, covenant monitoring, and stakeholder reporting.

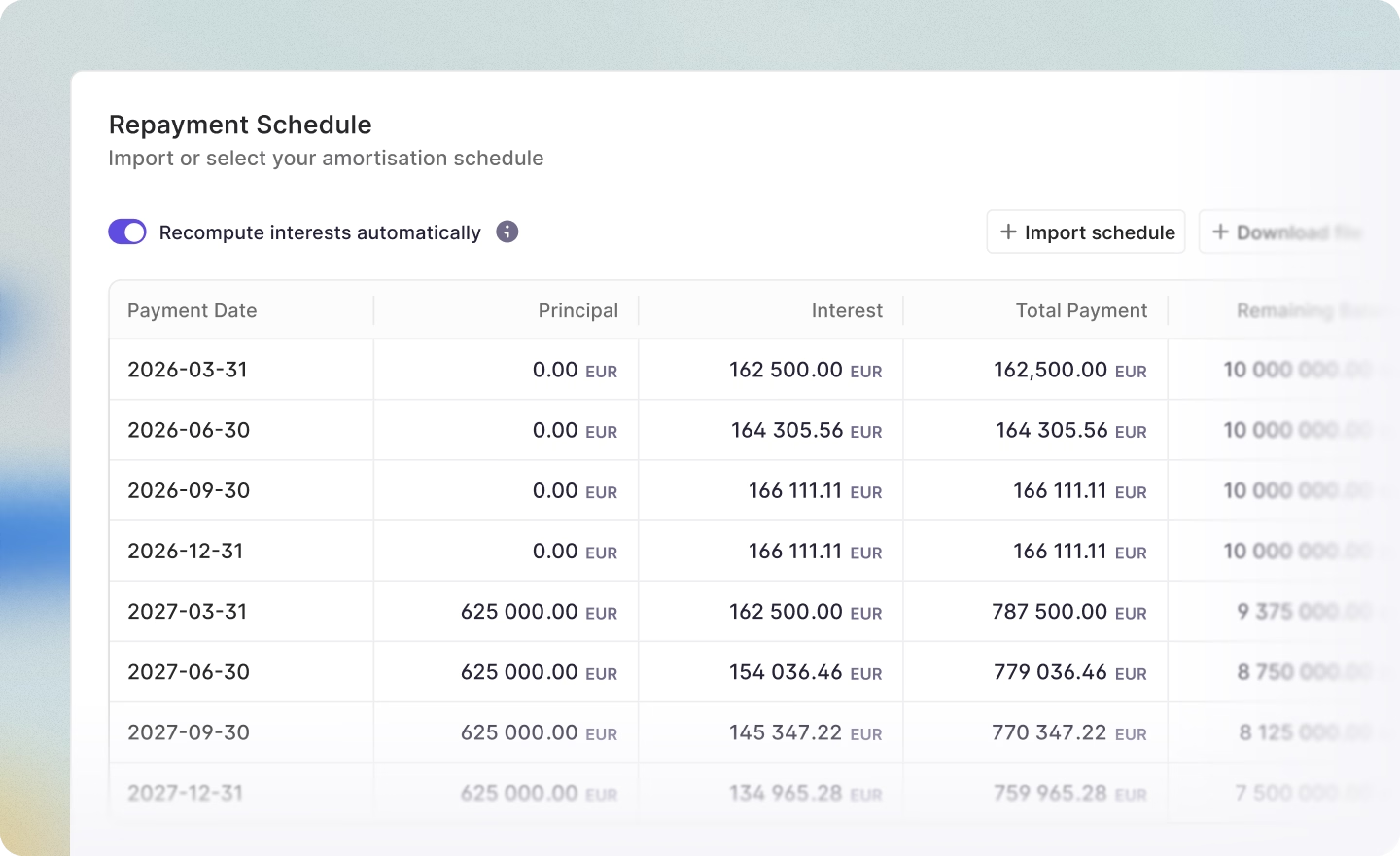

Step 4: Calculate and monitor interest obligations

Once loans are registered, the treasury team must track ongoing interest obligations accurately. For fixed-rate debt, this is straightforward—the interest amount is known in advance. For variable-rate debt, interest calculations require more attention.

The key inputs to a variable-rate interest calculation are:

- The applicable benchmark rate at the most recent reset date (e.g., three-month EURIBOR as of the rate-fixing date)

- The margin (or spread) above the benchmark, as specified in the loan agreement

- The day-count convention, which determines how the number of days in an interest period is calculated. Common conventions include Actual/360 (used for EURIBOR-based loans), Actual/365 (used for SONIA-based loans), and 30/360 (used for most fixed-rate corporate bonds and some fixed-rate loans, assuming 30-day months and a 360-day year)

- The interest period (e.g., monthly, quarterly, semi-annually)

- Any floor on the benchmark rate, which sets a minimum even if the published rate is lower

For example, a €10 million loan at three-month EURIBOR + 2.00% with an Actual/360 day-count convention and a 91-day interest period would be calculated as: (Principal × (EURIBOR + Margin) × Days in Period) / 360.

Automating these calculations, rather than relying on manual spreadsheet updates, reduces errors and ensures that your cash flow forecasts always reflect the latest rate environment.

Step 5: Integrate debt into cash flow forecasting

Debt servicing costs, comprising both interest payments and principal repayments, are often among the largest line items in a company's cash outflow forecast. Integrating debt data directly into your cash flow forecasting model ensures that upcoming obligations are accurately reflected in your projected cash position.

In a 13-week cash flow forecast, debt-related outflows should typically appear as distinct line items, separating interest payments from principal repayments, within the outflow section of the forecast. This granularity helps treasury teams identify periods where debt payments coincide with other large outflows (such as payroll, tax, or supplier payments) and take action to ensure sufficient liquidity.

For companies with variable-rate debt, forecasting also involves projecting future interest costs under different rate scenarios—typically a base case, an upside scenario (rates fall), and a downside scenario (rates rise). The impact compounds quickly at scale: a 100 basis point increase in EURIBOR on a €50 million floating-rate loan increases annual interest expense by €500,000. This kind of scenario analysis helps treasury teams understand rate sensitivity, inform hedging decisions, and prepare accordingly, particularly when hedging instruments are not tracked alongside the underlying debt, making net exposure hard to assess.

Step 6: Monitor covenant compliance

Financial covenants are conditions embedded in loan agreements that require the borrower to maintain certain financial metrics. Breaching a covenant, even a technical breach with no immediate financial consequence, can erode lender confidence, trigger reporting obligations, and in severe cases lead to acceleration of repayment or default.

The most common financial covenants include:

- Leverage ratio (Net Debt / EBITDA): Limits how much debt the company can carry relative to its earnings. A typical threshold might be 3.0x or 4.0x, meaning total net debt cannot exceed three or four times EBITDA.

- Interest coverage ratio (EBITDA / Interest Expense): Ensures the company generates enough earnings to service its interest payments. A common minimum is 2.0x or 3.0x.

- Minimum liquidity: Requires the borrower to maintain a minimum level of cash or available credit facilities at all times.

- Net debt cap: Sets an absolute ceiling on the company's total net debt.

- Capital expenditure limits: Restricts the amount the company can spend on capital investment in a given period.

Monitoring covenants requires up-to-date financial data, not just from your debt register but from your accounting and treasury systems as well. Companies typically test covenants quarterly, aligned with their financial reporting cycle. A centralized platform that combines debt data with real-time cash positions and financial metrics makes this significantly more manageable.

Best practice is to track covenant headroom—the difference between the actual metric and the covenant threshold—on an ongoing basis, rather than only at test dates. This early warning system gives treasury teams time to take corrective action (such as reducing discretionary spending, accelerating receivables, or negotiating a temporary waiver with lenders) before a breach occurs. It's worth noting that non-financial covenants, such as negative pledge clauses that can be triggered by corporate restructurings or asset disposals, are a common and often overlooked cause of default events, and deserve the same proactive tracking.

Step 7: Manage debt maturity and refinancing

As loans approach maturity, treasury teams must plan for repayment or refinancing well in advance. A maturity profile, showing when each debt instrument comes due, is an essential planning tool.

Key considerations when managing maturities include:

- Avoiding maturity concentration: Having too many loans maturing in the same period creates refinancing risk. Aim to stagger maturities across different time periods.

- Monitoring market conditions: The cost and availability of refinancing depend on prevailing interest rates, credit market conditions, and the company's own creditworthiness. Starting refinancing conversations early (typically 6–12 months before maturity) gives the treasury team more options.

- Evaluating prepayment: Some loans can be repaid early, but prepayment may trigger fees (known as breakage costs for variable-rate loans, or make-whole premiums for fixed-rate instruments). The treasury team should weigh these costs against the benefit of reducing outstanding debt.

Maintaining banking relationships: Regular communication with lenders builds trust and can lead to more favorable terms.

Step 8: Build reporting and stakeholder visibility

CFOs, board members, auditors, lenders, and investors all need visibility into the company's debt position. Effective debt reporting should clearly present:

- Total debt outstanding by instrument type, currency, and entity

- The maturity profile (when each instrument falls due)

- The split between fixed and variable-rate debt

- Current all-in cost of debt

- Covenant compliance status and headroom

- Hedging positions and their effectiveness

- Upcoming interest and principal payments

A well-structured debt report, updated regularly and easily accessible, builds confidence among stakeholders and supports better decision-making. Modern treasury platforms generate these reports from centralized data, reducing the manual effort of assembling information from multiple sources.

Managing intercompany (internal) debt

An intercompany loan is a loan between two entities in the same corporate group, for example a parent funding a subsidiary or one subsidiary lending surplus cash to another. The lender books a receivable and recognizes interest income; the borrower books a payable and interest expense. The concept is straightforward, but managing intercompany debt brings regulatory, tax, and operational complexity that external debt does not.

Intercompany loans serve several important purposes:

- Liquidity management: Moving surplus cash from entities that have it to entities that need it, without resorting to external borrowing. This is closely linked to broader cash management and cash pooling strategies.

- Capital allocation: Funding growth initiatives, acquisitions, or capital expenditure in specific subsidiaries.

- Working capital support: Providing short-term financing to cover operational cash flow gaps in subsidiaries that may not have their own external credit facilities.

- Tax-efficient financing: Structuring intercompany lending to optimize the group's overall tax position. For example, by locating debt in jurisdictions with favorable interest deductibility rules (subject to strict compliance requirements).

- Foreign exchange management: Managing FX exposure by denominating loans in specific currencies to create natural hedges within the group.

Step 1: Assess the need and compare alternatives

Before establishing an intercompany loan, consider whether it's the most appropriate mechanism. Alternatives include equity contributions (injecting capital rather than lending it), dividend distributions (moving cash between entities by distributing profits), management fees (charging one entity for services provided by another), or having the subsidiary borrow externally. Each option carries different implications for tax, balance sheet structure, and regulatory compliance.

Key questions to evaluate:

- Does the borrowing entity have a genuine, documented need for the funds?

- Is the lending entity in a position to provide the funds without compromising its own liquidity?

- How does the cost of an intercompany loan compare to the subsidiary borrowing from an external bank?

- What are the tax implications in both the lender's and borrower's jurisdictions (interest deductibility, withholding taxes, transfer pricing)?

- Does the corporate group have a formal intercompany financing policy in place?

Step 2: Set arm's-length terms

Transfer pricing regulations in most jurisdictions require that intercompany loans be structured at arm's length. The OECD's Transfer Pricing Guidelines for Multinational Enterprises and Tax Administrations provide the international framework, and most countries have adopted some version of these rules.

Setting arm's-length terms involves:

Interest rate benchmarking

The rate charged on an intercompany loan should be comparable to what a third-party lender would charge the borrowing entity, taking into account the borrower's credit profile, the loan amount, tenor, currency, and whether the loan is secured. Common approaches include referencing published benchmark rates (e.g., EURIBOR or SOFR) plus an appropriate credit spread, or using transfer pricing databases that compile comparable loan transactions.

Repayment schedule and maturity

Define a realistic repayment schedule that aligns with the borrower's expected cash flows, and set a defined maturity date. Tax authorities may challenge loans with indefinite terms or no realistic repayment prospect as lacking economic substance, potentially reclassifying them as equity contributions, which would eliminate interest deductibility for the borrower and convert interest income to dividend income for the lender.

Security

Decide whether the loan will be secured against specific assets. This decision affects the arm's-length interest rate, since secured loans typically carry lower rates than unsecured ones.

Step 3: Document the loan formally

Formal documentation is the foundation of tax compliance and audit readiness for intercompany loans. Tax authorities can, and regularly do, reclassify the loan as an equity contribution.

The loan agreement should include, at a minimum:

- Names and registered details of the lending and borrowing entities

- Loan amount and currency

- Interest rate, including the basis for calculation and reset frequency (if variable)

- Day-count convention for interest calculations

- Repayment schedule and maturity date

- Any security or collateral arrangements

- Events of default and remedies

- Governing law and jurisdiction

The agreement should be signed by authorized representatives of both entities and stored in a centralized document management system alongside the group's transfer pricing documentation.

Step 4: Record, calculate interest, and reconcile

Both entities must record the loan on their books: the lender as a receivable, the borrower as a payable. Interest accruals should be calculated and posted at the agreed intervals (typically monthly or quarterly), using the same methodology and rates on both sides.

Regular reconciliation between the lender's and borrower's records is essential. Discrepancies, which commonly arise from timing differences in posting, different FX rates used for translation, or simple data entry errors, should be identified and resolved promptly. Ideally, this happens as part of a monthly close process rather than being left to quarter-end or year-end.

For group financial consolidation, intercompany loans and the associated interest income and expense must be eliminated. The receivable on the lender's books and the payable on the borrower's books should net to zero. Discrepancies at consolidation are one of the most common causes of delayed month-end closes in multi-entity groups.

Step 5: Monitor ongoing compliance and exposure

Intercompany loans are not "set and forget." Treasury teams should continuously monitor:

- Outstanding balances and payment schedules across all intercompany loans in the group

- Interest rate updates for variable-rate intercompany loans (using the same benchmark update process as for external debt)

- FX exposure on cross-currency intercompany loans, which can create material gains or losses for both entities as exchange rates move

- Arm's-length pricing validity, particularly if market conditions or the borrower's financial position change materially. Many tax authorities require periodic (typically annual) transfer pricing studies to substantiate intercompany loan terms.

- Thin capitalization limits in the borrower's jurisdiction, which may cap the amount of intercompany interest that is tax-deductible

- Withholding tax obligations on interest payments, which vary by jurisdiction and may be reduced or eliminated by applicable tax treaties

- Actual repayment activity, since a loan that is never repaid risks reclassification as equity by tax authorities

Common challenges with intercompany debt

Spreadsheet reliance

Many finance teams still track intercompany loans in spreadsheets, which leads to formula errors, version control problems, and a lack of audit trail. As the number of entities and loans grows, the risk of misstatement increases.

Mismatched balances

The lender and borrower frequently record different balances for the same loan, which surfaces during reconciliation and can delay the month-end close. Establishing a single source of truth, where both entities reference the same loan record, is the most effective way to prevent this.

Non-arm's-length terms

If the interest rate or other terms on an intercompany loan don't reflect what unrelated parties would agree to, tax authorities may adjust the taxable income of one or both entities. This risk increases when rates are set informally or not updated to reflect changing market conditions. Regular benchmarking against published reference rates and comparable third-party transactions is essential.

Missing or incomplete documentation

Without a formal loan agreement specifying all material terms, tax authorities may reclassify the loan as an equity contribution. Standardized loan agreement templates, enforced consistently across the group, help prevent this.

Untracked FX exposure

When intercompany loans are denominated in a currency other than the functional currency of either entity, exchange rate movements can create significant unrealized gains or losses. Without centralized tracking, these exposures may go unhedged and unmonitored, introducing volatility into both entities' financial results.

Poor visibility into cash impact

Intercompany debt obligations are sometimes excluded from the group's cash flow forecast, creating blind spots in liquidity planning.

Best practices for debt management

These practices apply to both external and intercompany debt, reflecting the approaches used by treasury teams managing complex, multi-entity debt portfolios.

Centralize your debt register

Keep all debt, external and intercompany, in one register. It underpins accurate interest calculations, forecasting, covenant monitoring, and audit readiness (see Step 3 under Managing external debt).

Automate interest and repayment calculations

Manual calculations are a persistent source of error, especially for variable-rate loans whose rate resets periodically. Automating them, and feeding the results into your forecast, keeps projections in step with the latest rates. For EURIBOR-linked loans, that means pulling in the daily rate publications automatically.

Integrate debt data with cash flow forecasting

Treat debt servicing as a first-class line item in your forecast, for both external and intercompany debt (see Step 5 under Managing external debt).

Use scenario analysis for rate exposure

For material variable-rate debt, model the effect of a 50, 100, or 200 basis point move in your benchmark rate on interest expense and cash outflows. This informs hedging decisions and gives the CFO and board a clear read on rate sensitivity.

Maintain rigorous documentation standards

Every loan needs a signed agreement on file, with all amendments, waivers, rate changes, and covenant calculations stored centrally. For intercompany loans, this underpins transfer pricing compliance; for external debt, it supports covenant reporting and lender communication.

Conduct periodic portfolio reviews

Review the full portfolio at least quarterly. Check whether refinancing could lower costs, whether the fixed and variable mix still fits the environment, whether intercompany terms still reflect market rates, and whether covenant headroom is sufficient. Involve treasury, FP&A, and tax.

Build stakeholder-ready reporting

Standardize reporting on total debt, maturity profiles, interest costs, covenant metrics, and currency exposure, for the board, lenders, auditors, and investors. A centralized platform generates these from live data.

How Atlar supports debt management

Most of the challenges in this guide, from tracking loans in spreadsheets to recalculating variable-rate interest by hand, come down to one thing: debt data sitting apart from the cash, payments, and forecasts it relates to.

Atlar's Debt Management suite brings debt into the same platform that finance teams already use for cash management, payments, forecasting, and reconciliation—with automated interest calculations, centralized documentation, and a full audit trail. Finance teams at companies like GetYourGuide, Acne Studios, and Lovable already use Atlar to manage their treasury operations. To learn more about debt management in Atlar, get in touch with our team.

_NEF-EDIT.avif)