Treasury as a Value Creation Lever in PE-Backed Companies

There is a version of treasury that costs money and a version that makes money. Most private equity (PE)-backed companies are running the first version. The gap between the two is measurable in EBITDA, exit multiple, and management hours, and it is closable within the hold period if you approach it correctly.

The PE Treasury Problem Is Different

Treasury in an independent company is a steady-state function. In a PE-backed company, the calculus changes on almost every dimension.

A mid-market PE hold typically runs 5–7 years, and every finance infrastructure decision needs to generate returns within that window. The strategies PE firms use to build value also create specific treasury stress points that an independent company rarely encounters.

Buy-and-build

A company executing an active acquisition strategy can absorb dozens of entities in a short period of time. One Atlar customer completed more than 60 acquisitions in under six months. Each acquired entity arrives with its own banking relationships, payment processes, and local finance team. The centralised group finance function is expected to have visibility across all of it, but in practice they often don't: access to acquired bank accounts is held locally, not handed over immediately, and integrating those accounts into the group's house bank takes months. Sensitive operational processes, like customer billing, may run through the acquired entity's existing accounts, creating reluctance to touch anything that risks disrupting revenue.

The result is a group running its capital allocation decisions on incomplete information. Without a consolidated view of cash across all entities, the CFO cannot confidently answer whether the business has the liquidity to fund the next acquisition, service debt, or accelerate a growth initiative from its own balance sheet — or whether it needs to draw on a credit facility to do so. Millions in excess cash sitting across acquired entity accounts that goes undeployed, while the group may simultaneously be paying interest on revolving credit it did not need to draw. A bank-level cash pool does not solve this; it only covers the house bank and primary accounts, not the fragmented estate of acquired entity accounts sitting outside it.

The right response is not to force all accounts into a single bank immediately. It is to connect everything to a single visibility layer first, illuminate the full cash position in real time, and then work through consolidation progressively. Critically, the platform needs to be able to connect new accounts at least as fast as the business acquires them. If it cannot, it becomes a bottleneck on the M&A strategy itself.

International expansion and structural change

As companies enter new markets, banking relationships tend to be established based on what is convenient locally rather than what is scalable for the group. A country manager or local finance lead opens an account with a regional bank that works well for local payroll and supplier payments. The central treasury team is often not involved in that decision, and sometimes cannot be: access to the account may require a locally-issued bank token, or a national identification number held by someone in-country. The central team ends up with accounts on their balance sheet that they cannot see into directly.

The result at group level is the same fragmentation problem as buy-and-build, compounded by the fact that the local teams did not intend to create an opacity problem — they were solving a practical need. Carve-out situations add further pressure: TSA clocks give finance teams 90–180 days to stand up treasury operations that were previously handled by a parent company, by which point the combination of new entities, new geographies, and inherited banking relationships can be significant. The common thread across all of these scenarios is connectivity. Every new entity, geography, or structural change adds accounts that need to be visible to the central team before any active treasury management can happen.

Lean teams and cash efficiency

Operating partners will not approve a treasury headcount build-out. The expectation is that the existing finance team delivers treasury-grade output without a dedicated treasury organisation. That constraint has a direct cash flow dimension that is often underweighted in the business case for treasury infrastructure. A well-run treasury function does not just reduce cost, it actively generates return. Cash that is not pooled and put to work sits idle in operating accounts earning nothing, when it could be deployed into money market funds or short-term fixed deposits. The amount varies by company size and business model, but the return is material: at Mangopay, an Advent International portfolio company, €20M of excess cash was identified and put to work, generating 6.1x ROI on the technology investment from yield alone, flowing directly into free cash flow. It is an investment return the business is either capturing or not, and it compounds across the hold period.

The challenge underneath the others

Treasury is rarely the only finance challenge in a PE-backed company, but it is often the one that sits underneath the others. The cost of poor treasury infrastructure is not just operational friction. When cash reporting is slow, the CFO and operating partner are making capital allocation decisions on incomplete information. When idle cash is not being actively managed, the business is carrying an implicit financing cost on every growth initiative it funds from its own balance sheet. When payment processes are manual and approval chains are informal, the finance team's time is consumed by execution rather than analysis. The cumulative effect is a business that is not operating at full capacity — one that may have to deprioritise investments, defer initiatives, or delay decisions simply because the financial infrastructure cannot keep pace with the strategic agenda. Treasury is not a back-office function in a PE-backed company. It is load-bearing infrastructure for the value creation plan.

Why the Existing Options Don't Work

Finance leaders who recognise the gap typically look at three options. Each has a structural problem.

Spreadsheets and bank portals work until the first acquisition or the first new geography or when you hit 3+ banks being used. Then they fail suddenly, usually at the worst possible moment.

Enterprise treasury management systems built over the past two to three decades were designed for a specific user: a dedicated treasury professional at a large corporate, managing a full treasury function with analysts, IT support, and years of platform experience. These systems reflect that complexity. They handle multi-bank global connectivity, sophisticated hedging programs, and derivative accounting across hundreds of entities. For a Global 500 group treasurer with a team behind them, that depth makes sense.

For a PE-backed mid-market company, it is overkill in the wrong direction. The platforms are built to be operated by specialist teams to warrant investment, and in practice they require long-standing treasury expertise just to navigate day to day. A CFO, controller, or head of finance without a treasury background will struggle to extract basic value from them, let alone configure and run them independently. Most PE-backed companies at the €50M–€500M range do not have that profile in-house, and hiring for it takes time they do not have.

The economics compound the problem. A typical enterprise TMS takes 12–18 months to implement. Payback periods from go-live run two or more years. A company that signs a contract in year one of a 5–7 year hold reaches positive ROI around year four at the earliest. The financial benefit accrues almost entirely to the next owner. No operating partner approves that business case, and no CFO should propose it.

The problem compounds if there is no treasurer in post. The conventional sequence — hire the person, let them select the platform, run the implementation — adds six or more months of recruitment and onboarding before implementation even starts. In a compressed hold, that sequence can consume three to four years of the value creation window before it produces anything.

The rational alternative is to invert the sequence. Deploy treasury technology first, operated by the existing finance team. Unlock cash visibility, payment automation, and yield on idle balances quickly, within the first 60–90 days of the hold. Bring in a treasurer later, as the business scales, to augment a functioning infrastructure rather than build one from scratch. Technology-first treasury is not a compromise. In a PE context, it is the correct order of operations.

What's Changed

The reason technology-first treasury is now viable — and wasn't five years ago — is a convergence of three shifts.

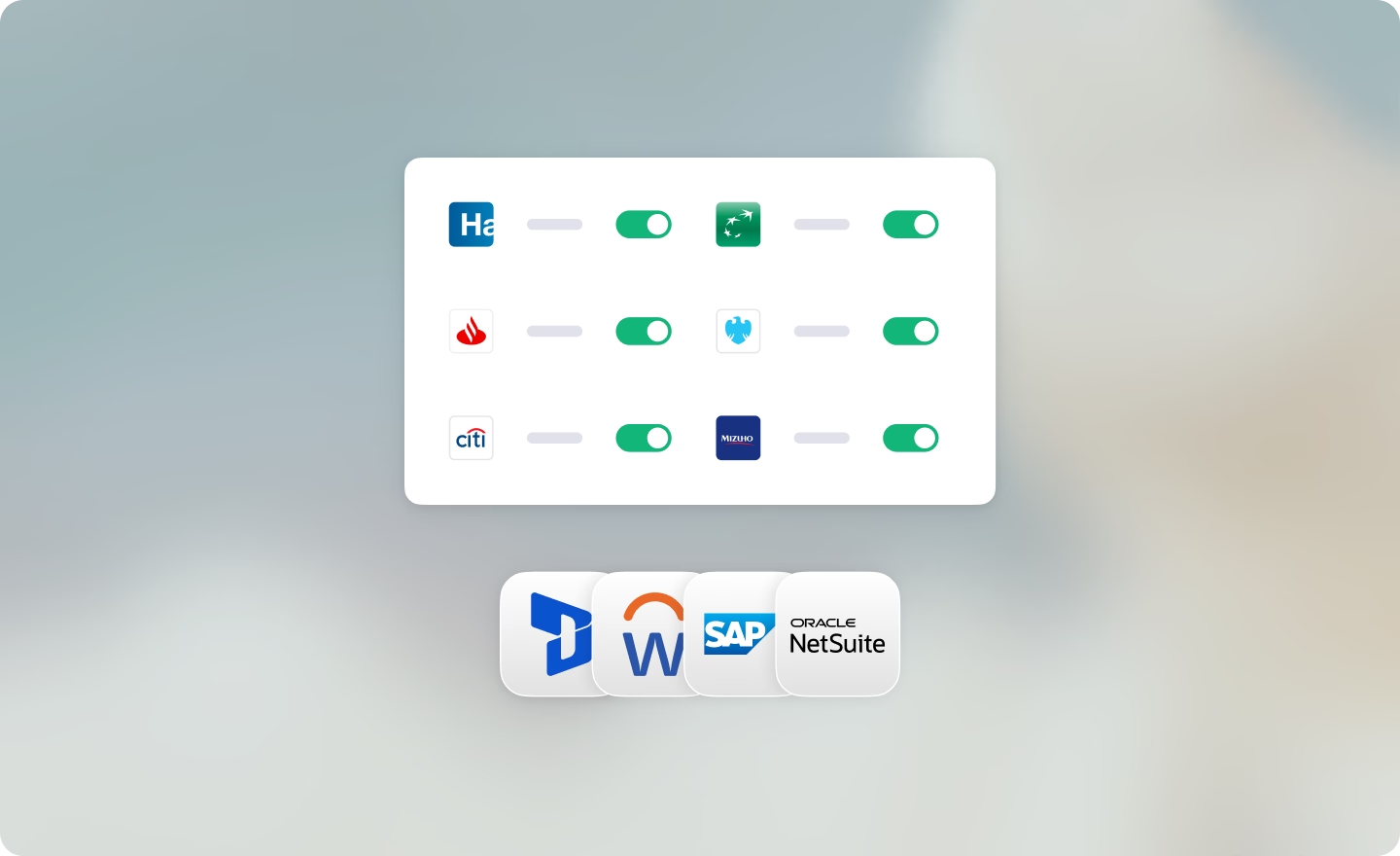

Connectivity as a managed service

The foundational barrier has always been bank connectivity. Getting a treasury platform to talk to multiple banks across multiple countries required IT resources, middleware vendors, and ongoing maintenance. The model that changes this treats connectivity as a fully managed service: the platform owns the connectivity layer, maintains the bank relationships, and handles protocol management. The customer's IT team is not in the critical path. When a portco acquires a new entity or opens accounts in a new country, connecting them is a configuration task, not a project. That distinction matters enormously in a buy-and-build strategy where the pace of acquisition cannot wait on implementation timelines.

ERP-native integration

Treasury and ERP operating on the same live data layer, rather than periodic imports and exports, means the finance team stops reconciling backwards and starts managing forwards. Payments initiated in the ERP are visible in the treasury platform before they clear. Expected receipts match against incoming bank transactions automatically. The month-end close shrinks. Cash reporting assembles itself.

Finance AI agents grounded in live data

Most finance teams experimenting with AI today are using disconnected tools: generic AI assistants fed spreadsheet exports, working from data that is always incomplete and always stale. For treasury this is a structural limitation. Cash positions decay in hours. An agent that cannot see all your banks simultaneously, or lacks ERP context to know what payments are due tomorrow, produces answers that are wrong in the ways that matter most.

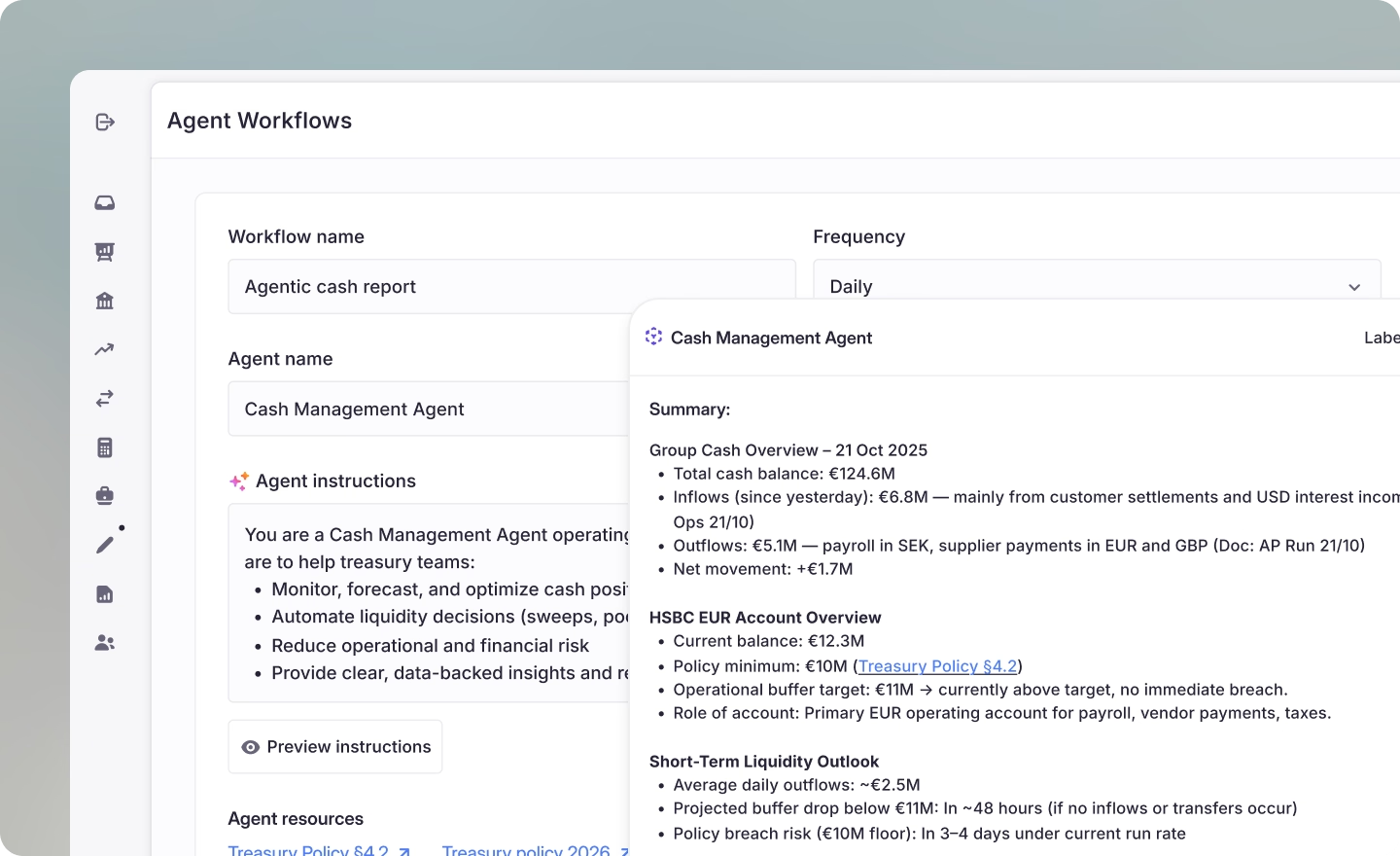

AI agents operating natively on live banking and ERP data simultaneously are a different category. A concrete example: a Daily Cash Position workflow runs automatically each morning. Before the CFO opens their laptop, it has already pulled balances across every account and entity, flagged unexpected transactions, matched settlements against expected receivables, calculated liquidity headroom by currency against treasury policy minimums, and drafted specific sweep proposals where thresholds have been breached.

The human-in-the-loop is central to the design. Routine tasks run autonomously. High-stakes actions — executing a sweep, releasing a payment batch, approving a transfer above a material threshold — surface to a named approver as a specific recommended action requiring explicit confirmation. The AI prepares the decision. The human executes it. Every action is logged with a full audit trail.

These workflows are configured in plain language by the finance team itself, with no IT involvement and no change orders. A portco that starts with Daily Cash Position can add a covenant headroom monitor or a weekly board cash commentary as the business grows. Each agent operates within explicitly defined, auditable data scopes. That is the answer to the governance question every operating partner and audit committee will raise.

The Atlar Case

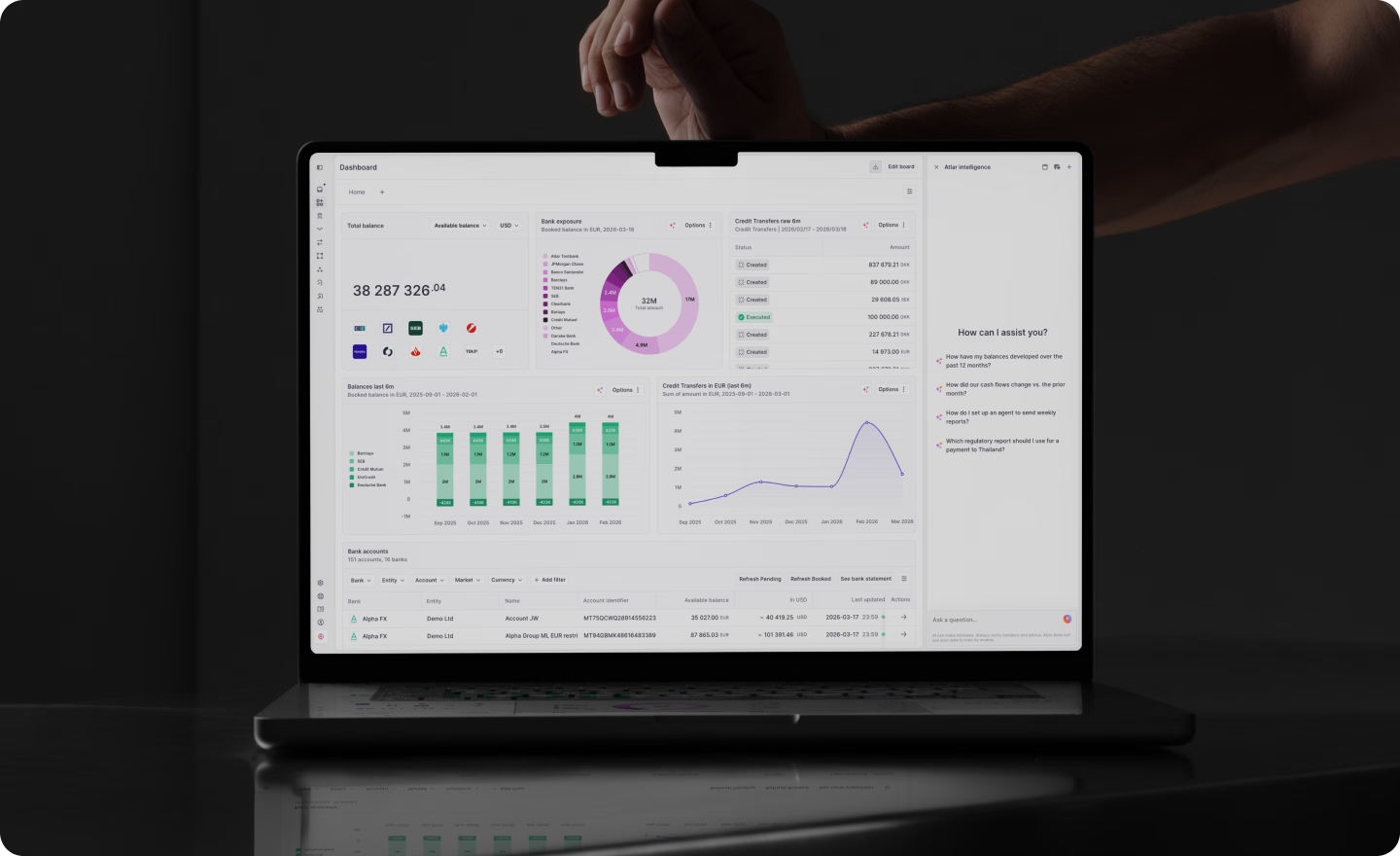

Atlar is a modern treasury management system built for mid-market companies on the model described above. Bank connectivity is fully managed: no IT dependency, no middleware, no third-party integrations. ERP integration is native and verified across NetSuite, Dynamics 365, SAP S/4HANA, Workday, and the new generation of AI-native ERPs. Deployment runs in under 90 days, inside the 100-day plan window, operated by the existing finance team.

The AI workflows described above, including Daily Cash Position, Payment Batch Review, Forecast Variance, Variance Analysis, are live features in production use at companies where the primary treasury user is a controller or a CFO, not a dedicated treasurer. When a treasurer eventually joins, they inherit a functioning infrastructure with a complete historical record and spend their time on strategy rather than foundation-building.

On the economics: that same Mangopay return, yield on idle cash flowing straight to free cash flow, landed inside the first year rather than year four, and came alongside more than 1,000 hours of annual treasury work automated.

For PE sponsors deploying across a portfolio, Atlar structures a master commercial agreement at the fund level. Each portco signs an order form on pre-agreed terms. Rollout is sequenced by treasury maturity and value-creation priority. Sponsors receive aggregate visibility into treasury KPIs across the portfolio.

See Where Your Treasury Sits

Treasury teams at Mangopay, Tide, Zilch, Storytel, Epidemic Sound, Truelayer, and Trustly run Atlar across their global banking structures. On G2, Atlar holds a 5-star rating, the highest of any treasury management system on the platform, and is backed by Index Ventures and General Catalyst.

Book a demo to see where the gap sits in your portfolio and what closing it looks like, or reach out to our partnerships team at partnerships@atlar.com.